The key news is the fall in industrial inflation, the possible start of deflation (about the same picture in China).

A structural crisis can follow a deflationary or inflationary scenario. Experience 1930-32 frightened the US monetary authorities so much that they were ready to do anything to prevent a deflationary scenario (it is for this reason that the supporter of flooding the economy with "money from a helicopter", Greenspan's successor as head of the Fed, Benjamin Bernanke, received the nickname "Benya the Helicopter").

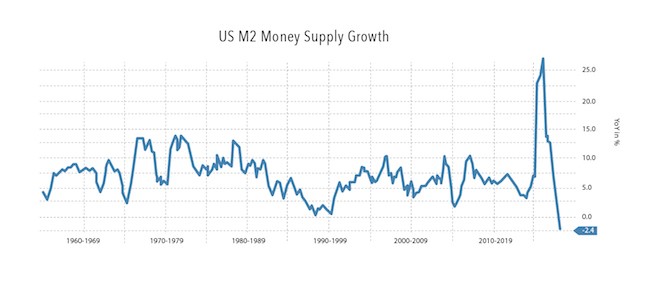

As experience has shown, raising the rate and other methods of tightening monetary policy (the Fed was actively reducing the money supply by selling securities on the balance sheet) gave a result, but not quite the expected result.

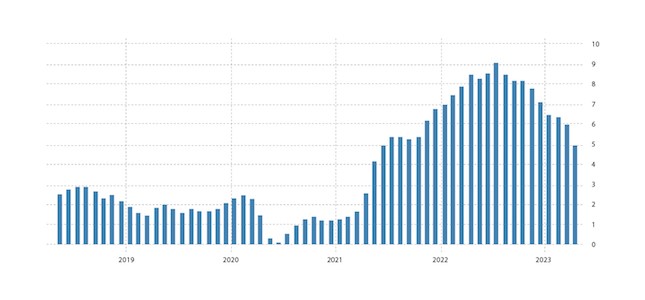

Consumer inflation has fallen, but clearly not enough:

Numerous experts are talking about this. For example, JPMorgan CEO Jamie Dimon: "People should be ready for higher rates for a longer period." But raising rates (or keeping the current ones) in the context of a declining economy will only lead to an acceleration of the recession. Which, we recall, has been going on for a year and a half and is hidden only due to an underestimation of inflation. However, it is possible that soon it will not need to be underestimated. Deflationary tendencies are growing.

Macroeconomics

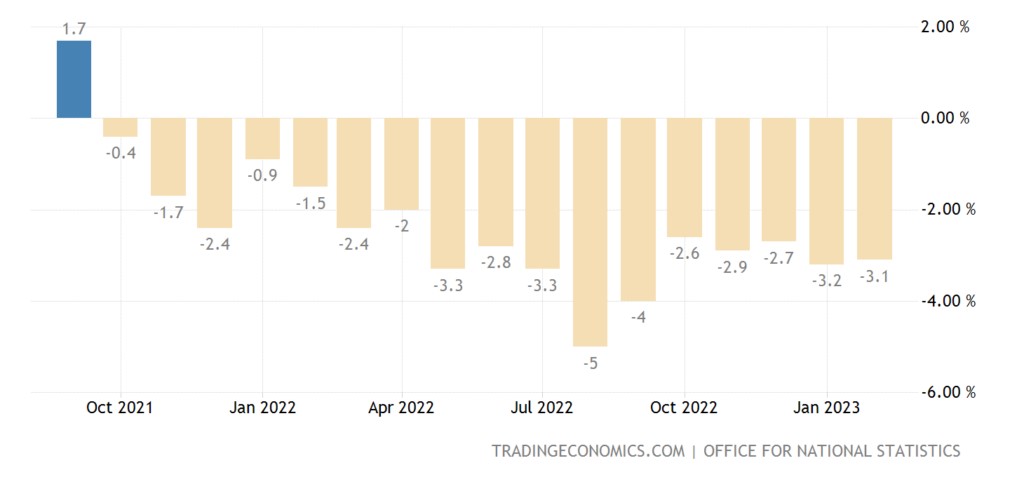

Industrial production in Britain -3.1% per year – the 17th consecutive minus:

Orders for machine tools in Japan -15.2% per year – the worst dynamics in 2.5 years:

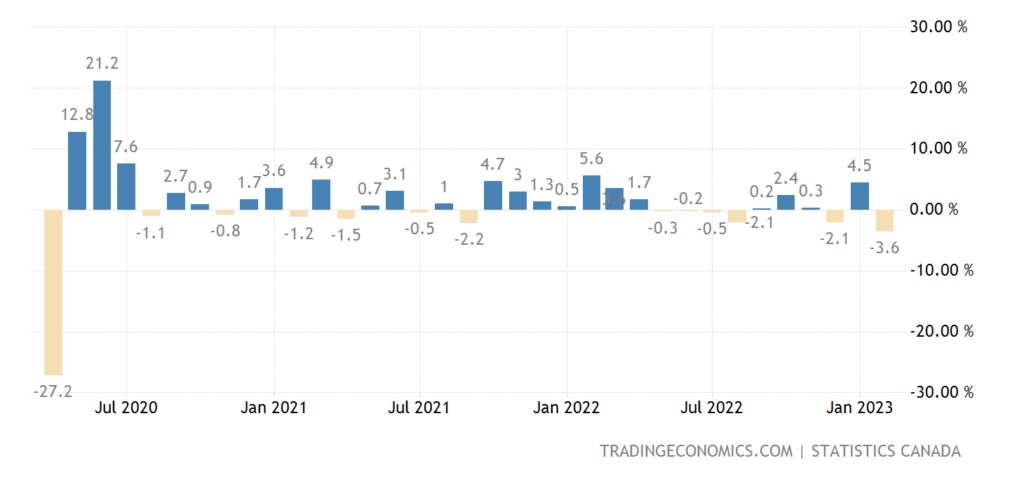

Manufacturing sales in Canada -3.6% per month – the strongest decline in 3 years:

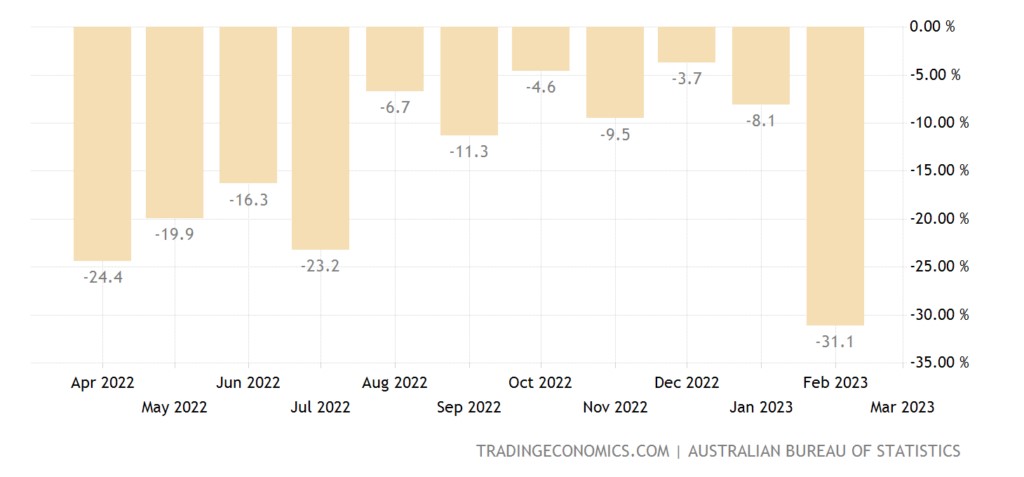

Building permits in Australia -31.1% per year – near record lows:

And their level rolled back to the values of 11 years ago:

The balance of house prices in Britain keeps in the red for 6 months in a row:

The average UK mortgage rate of 7.22% is a 15-year high:

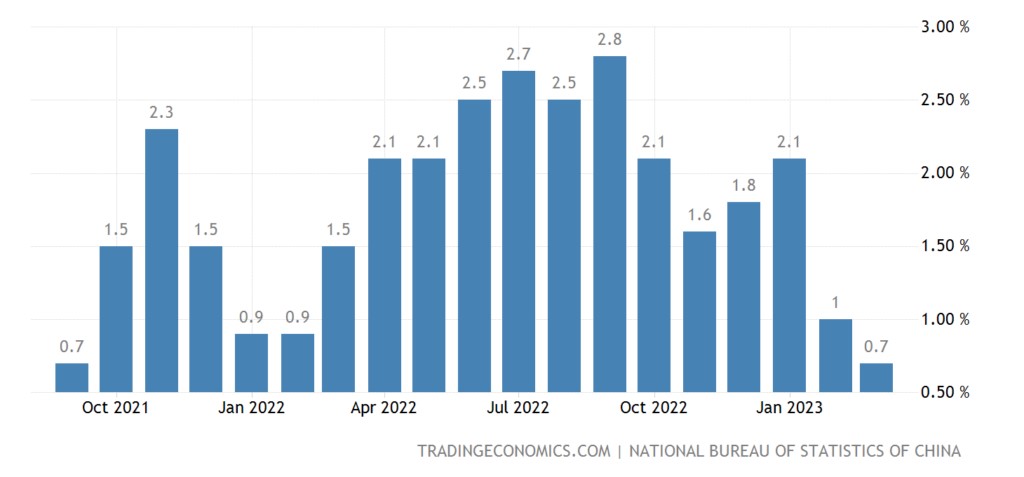

China CPI +0.7% per year – minimum for 1.5 years:

PPI China -2.5% per year – bottom in almost 3 years:

There is already almost obvious deflation, apparently, and the real sector has very serious problems.

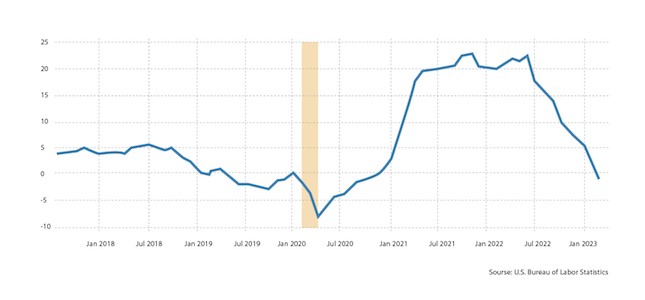

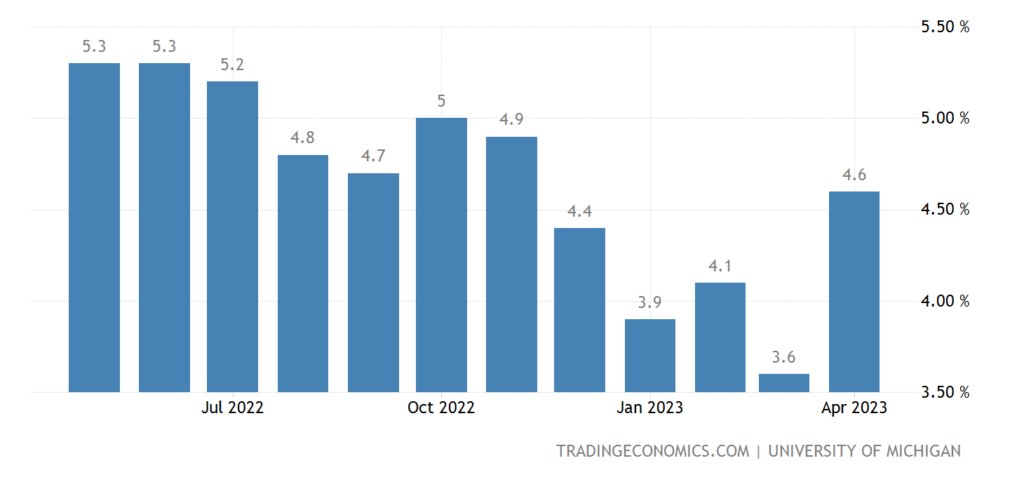

Inflation expectations in the US jumped to a 5-month high:

How does industrial inflation become deflation, consumer inflation somehow falls, and people expect prices to rise? But the fact is that there is some experience. As companies reduce prices amid falling demand, their debt grows. And, sooner or later, it comes to bankruptcies and / or closure of production, after which the remaining producers raise prices. This is no longer a market economy. This is an economy in falling markets, a completely different logic works.

Eurozone retail sales -3.0% per year – the most substantial decline in 2 years, the 5th negative in a row and the 8th in the last 9 months:

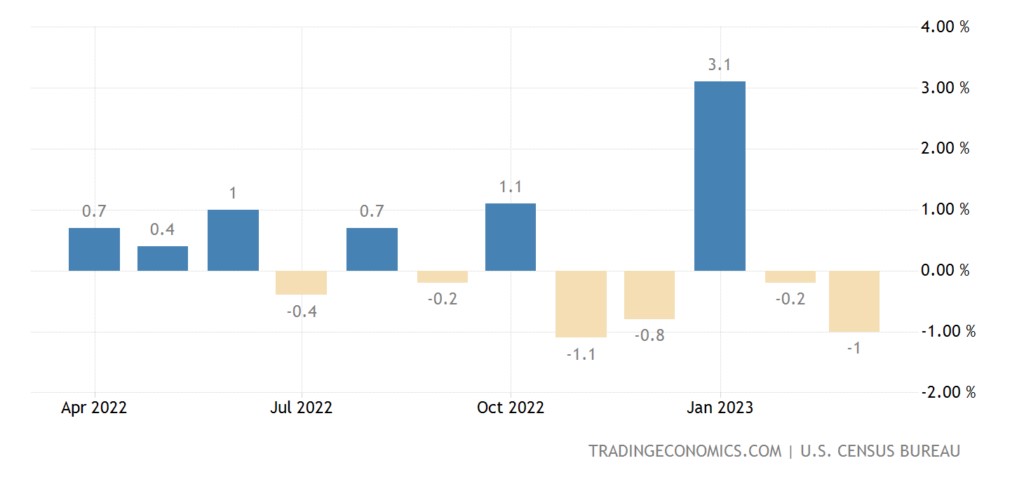

US retail -1.0% per month – 4th minus in the last 5 months:

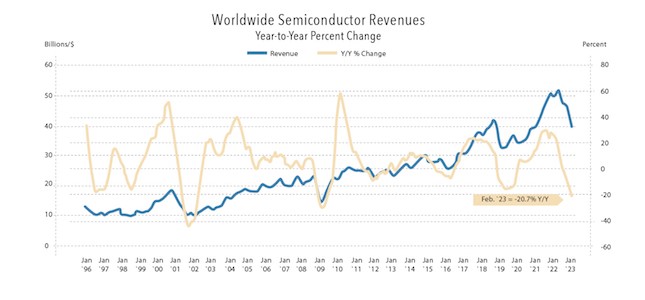

Global sales of semiconductors -20.7% per year – at least since 2009:

The Central Bank of South Korea left the monetary policy the same as the Central Bank of Canada. But the published minutes of the last meeting of the US Federal Reserve confirmed the readiness of the board to continue tightening monetary policy. The phenomenon of stagflation is already taking place (a decline in production against the background of still high, even nominal inflation, not like real inflation). Does Powell want to reinforce this trend? Well, he has the right. In the end, we are talking only about options for a recession. It still won't be possible to stop it!

As expected, after the banking crisis, which resumed issuance support for the financial sector, the banks are doing well:

JPMorgan reported a 52% increase in earnings to $12.62 billion, or $4.10 per share, for the three months that ended March 31. Excluding non-recurring costs, the bank earned $4.32 per share, beating analysts' average expectations of $3.41 per share.

Wells Fargo's net interest income rose 45% to $13.34 billion. The bank earned $1.23 per share, excluding non-recurring items, for the quarter that ended March 31. That's up from the average analyst estimate of $1.13 per share.

Citi earned $1.86 per share in the first quarter, beating the average analyst estimate of $1.67. Net income rose 7% to $4.6 billion, or $2.19 per share, from $4.3 billion, or $2.02 per share, a year earlier.

BlackRock, the world's largest asset manager, posted adjusted earnings of $7.93 per share. The consensus forecast was for payments of $7.76 per share.

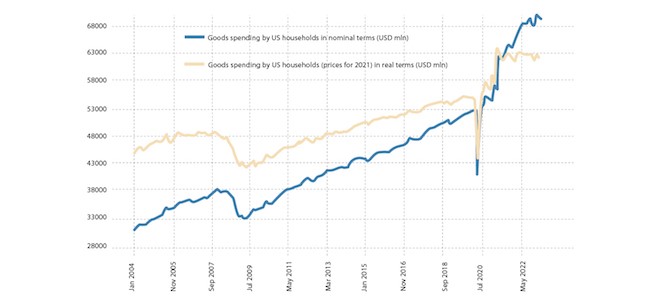

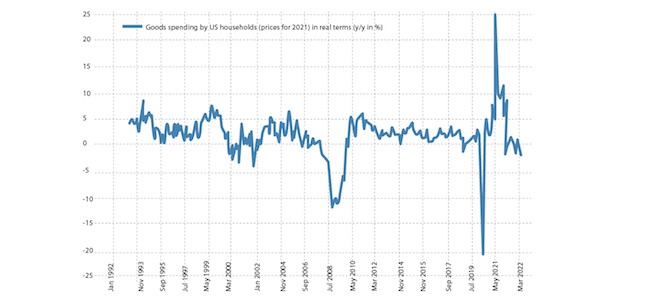

But for households, the picture does not look so optimistic:

And this is taking into account official inflation indicators. And if you take into account the real, then household spending will fall (compare with retail sales in the previous section).

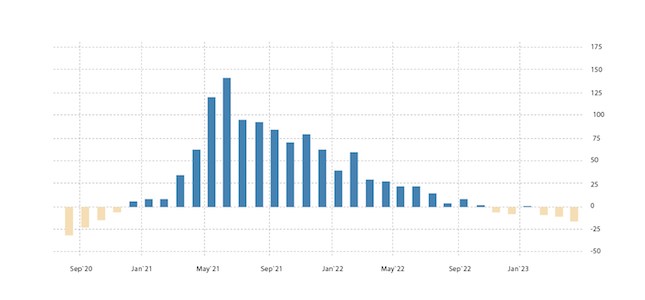

At the same time, the picture looks more and more distorted in the financial markets:

When the yield of "short" securities is greater than "long" ones, and for a sufficiently long time, we can safely say that the market is very unstable. Previously, this was generally an obvious sign of a recession, but now, when the entire system is in the "red” zone, there is no need to talk about any stable indicators. Involuntarily, investors begin to get nervous, which does not add stability.

Exhausted?")