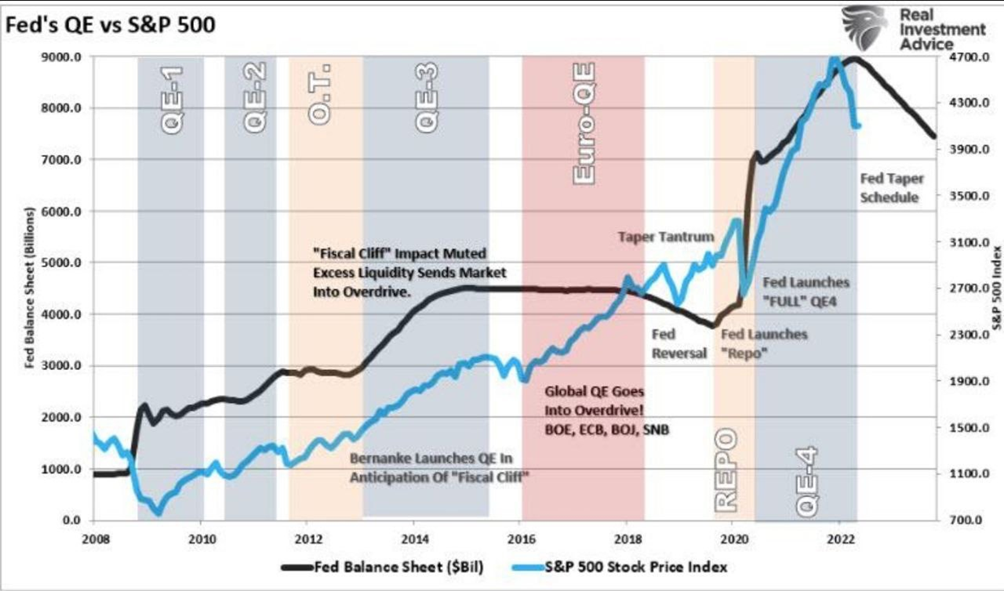

The main news of the week was that the head of the Fed, J. Powell, speaking at the Congress, disavowed the relationship between special operations in Ukraine and inflation in the US. This is not about the US and Russia, but about the fact that the head of the Central Bank goes against the logic of the head of the state, says that the US monetary authorities cannot find a single explanation for the causes of the inflation disaster. It should be noted that a similar situation exists in the European Union, and the ECB leadership is unable to present any coherent strategy based on analysis of the situation. At the same time, the feeling of catastrophe is growing, especially if we take into account the relationship between the money supply and the stock indices:

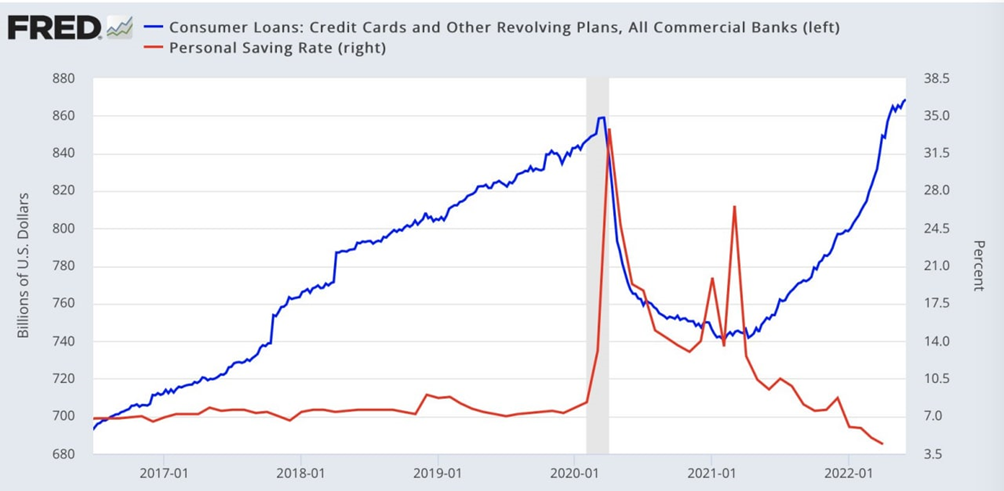

In other words, if the tightening continues (this is for the Fed, the ECB is milder for now), markets will collapse — actually, there is already a decline — but that is just the beginning. At the same time, aggregate demand and household savings are already going down, while their loans are growing:

If it is also assumed that the decline in demand is an automatic decline in GDP, the picture becomes even bleaker. Recall that since the fourth quarter of last year in the US began a full-fledged structural crisis, similar to the crisis of 1930-32 (the only difference is in the course of a disease — then it was under the deflationary scenario, and now it is on the inflationary one), and it will last a long time, not less than five years.

Judging by the speeches of the Fed leadership in recent days, its officials already realize this. They do not understand the mechanism of the crisis (although the book in which it’s expounded is on sale in the US in English), but have already realized that it is outside the standard “economics” tools. And today, the main task of all politicians and experts is not economic policy, but an attempt to avoid personal responsibility for the current situation.

Macroeconomics

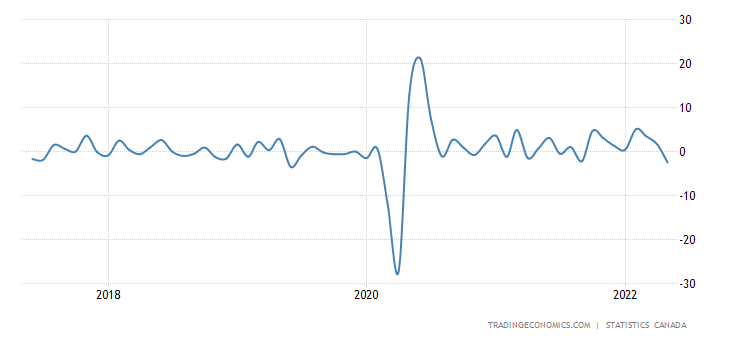

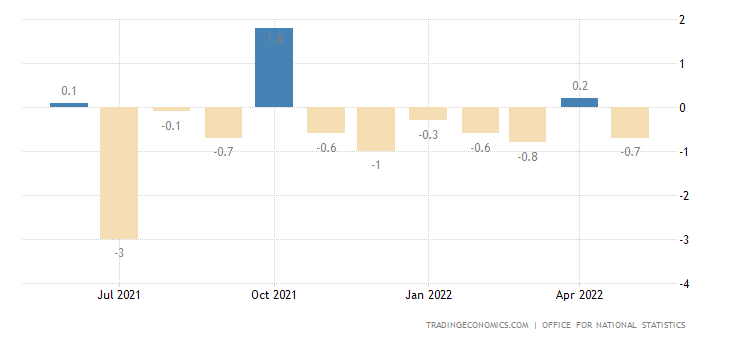

Sales in the manufacturing industry in Canada gave -2.5% per month — the worst performance in 2 years:

Canada Manufacturing Sales MoM

PMI (Purchasing Managers’ Index, industry peer review, it’s value below 50 means stagnation and recession) of the French industry is at the trough for 19 months:

France Manufacturing PMI

In Germany — in 23 months:

Germany Manufacturing PMI

In the Euro Area — for 22 months:

Euro Area Manufacturing PMI

In the US — for 23 months:

In Britain — for 23 months:

United Kingdom Manufacturing PMI

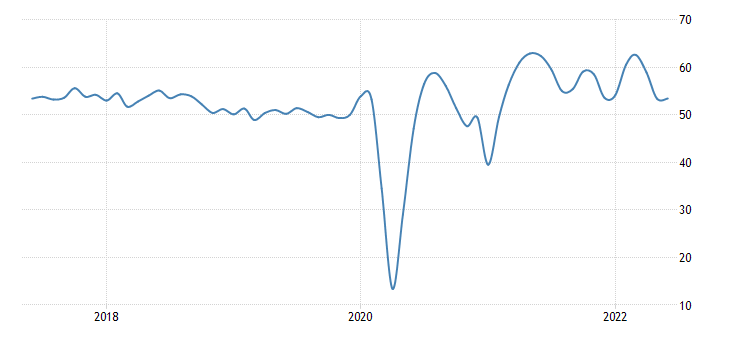

The latter also has the lowest service sector in 16 months:

United Kingdom Services PMI

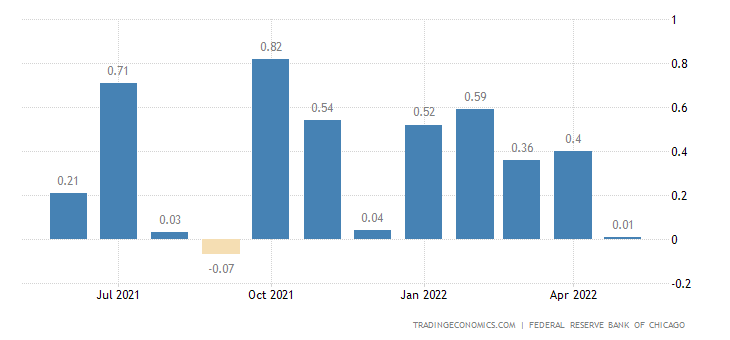

The National Activity Index in the US from the Chicago Fed has zeroed (an 8-month trough):

United States Chicago Fed National Activity Index

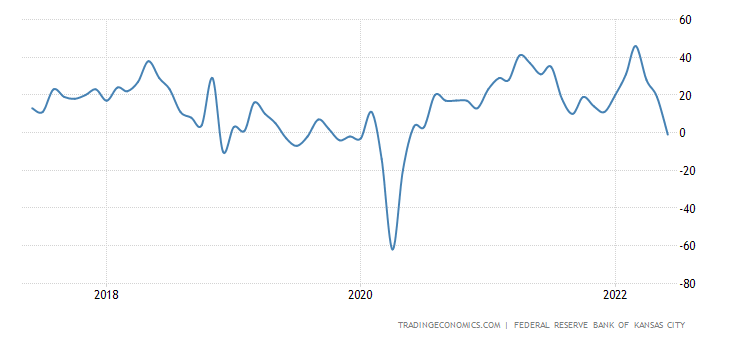

United States Kansas Fed Manufacturing Index is the weakest in 2 years and is already in the red zone:

United States Kansas Fed Manufacturing Index

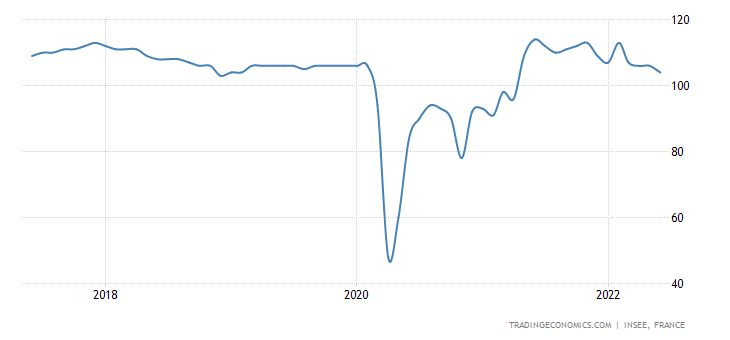

France Business Climate Composite Indicatore is at its lowest for 14 months:

France Business Climate Composite Indicator

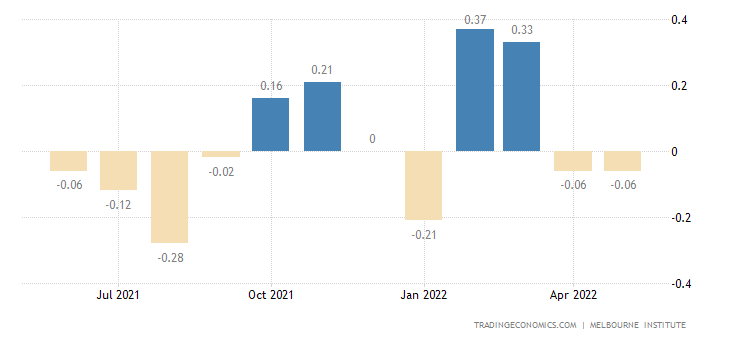

Australian leading indicators fall for two straight months:

Australia Leading Economic Index

As in Argentina, where they also plummeted at the fastest rate in 2 years (-2.0% per month):

Argentina Leading Economic Index

Inflation data, as usual, are on record.

CPI (Consumer Price Index) of Japan climbed to the top since 2014 (+2.5% per year):

Japan Inflation Rate

Less fresh food — since 2015 (+2.1% per year):

Japan Core Inflation Rate

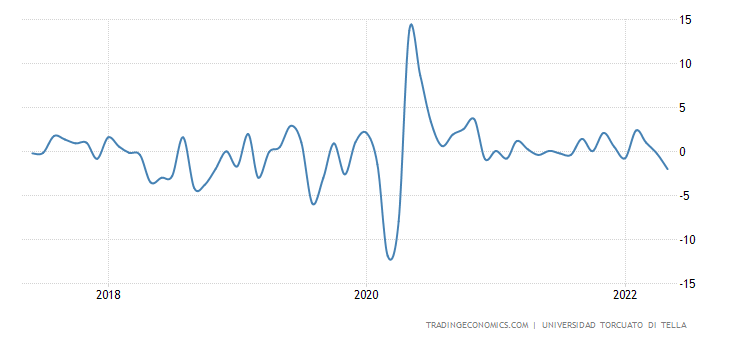

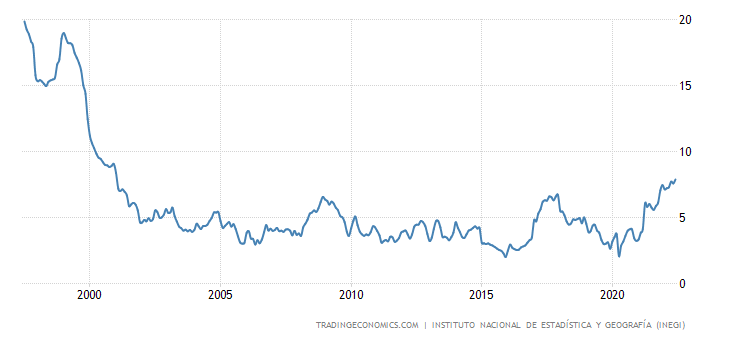

CPI Mexico +7.9% per year is the highest since 2001:

Mexico Mid-month Inflation Rate YoY

Mexico Mid-month Inflation Rate YoY

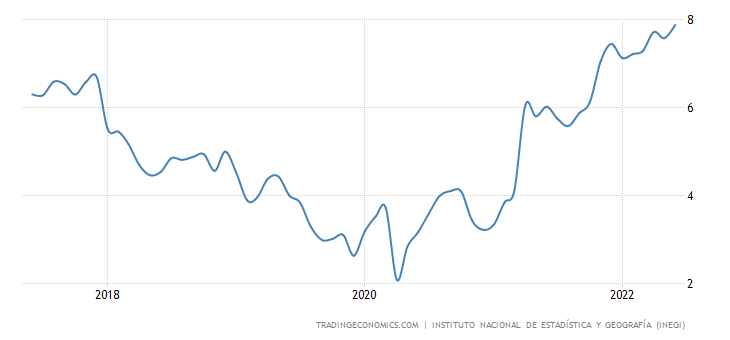

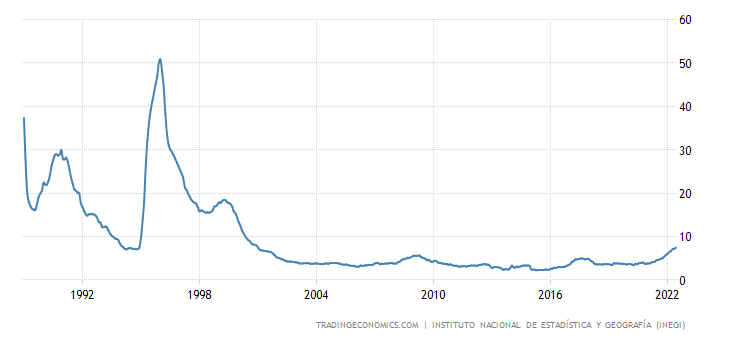

The same with the core inflation rate of +7.5%(excluding highly volatile food and energy components):

Mexico Mid-month Core Inflation Rate YoY

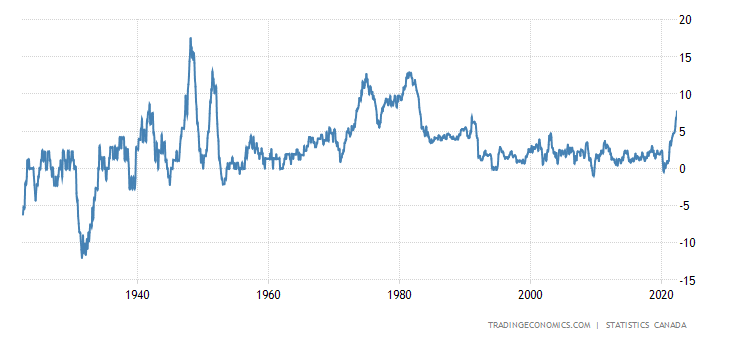

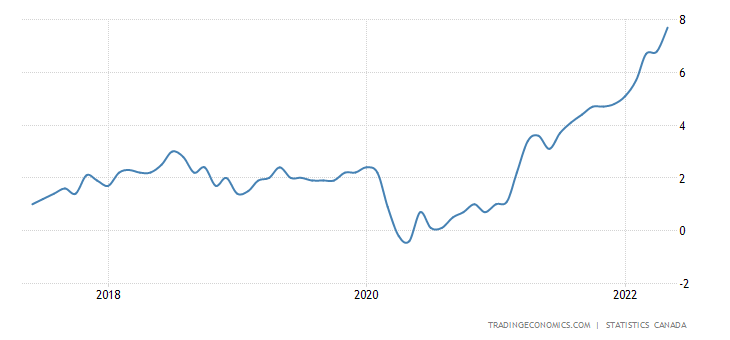

Canadian CPI +7.7% per year topped since 1983:

Canada Inflation Rate

Canada Inflation Rate

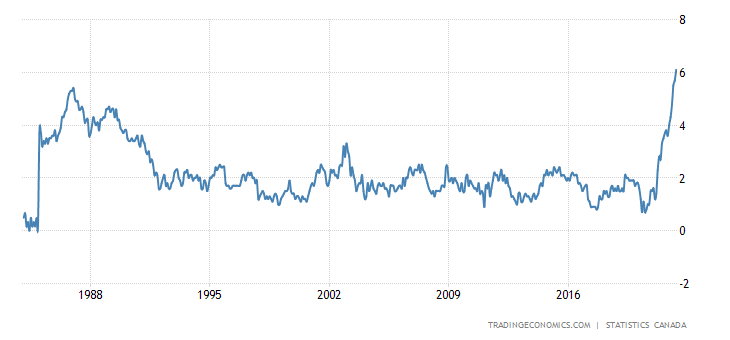

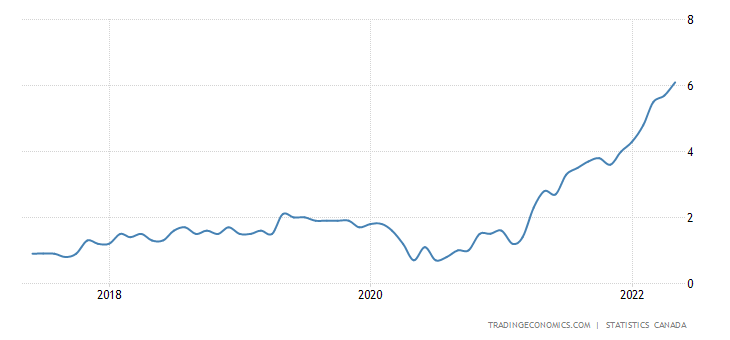

Less food and energy +6.1% per year, that’s a record for 38.5 years of statistics:

Canada Core Inflation Rate

Canada Core Inflation Rate

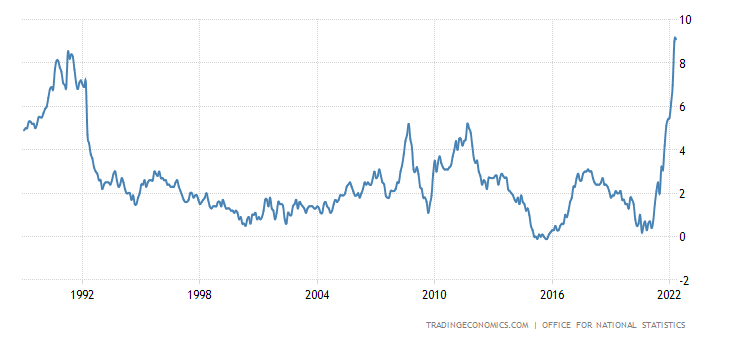

Britain’s CPI of +9.1% per year is the highest for 33.5 years of survey:

United Kingdom Inflation Rate

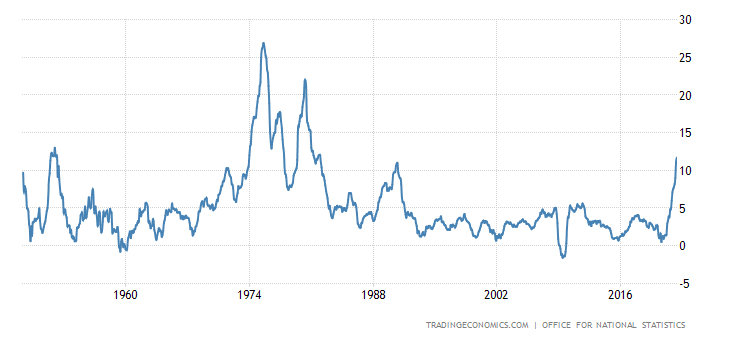

United Kingdom Retail Price Index +11.7% per year reached its highest level since 1981:

United Kingdom Retail Price Index YoY

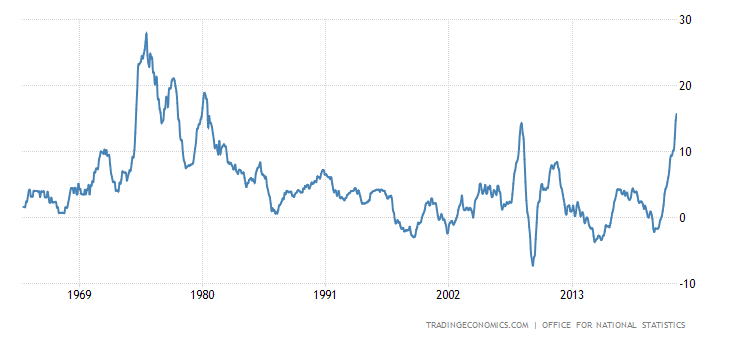

UK PPI (industrial inflation index) +15.7% per year, that’s the peak since 1980:

United Kingdom Producer Prices Change

United Kingdom Producer Prices Change

Core PPI +14.8% per year is a record high for 25.5 years of survey:

United Kingdom Core Producer Prices YoY

United Kingdom Core Producer Prices YoY

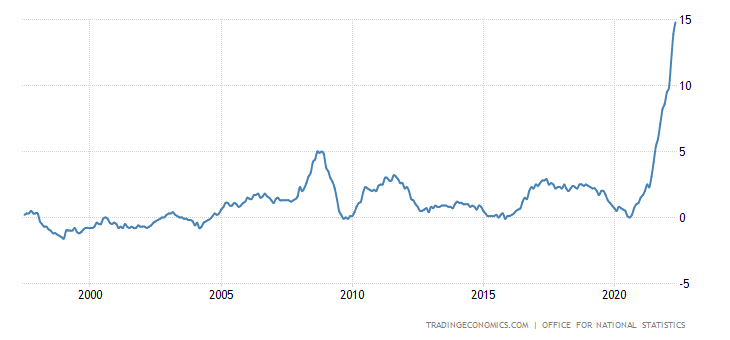

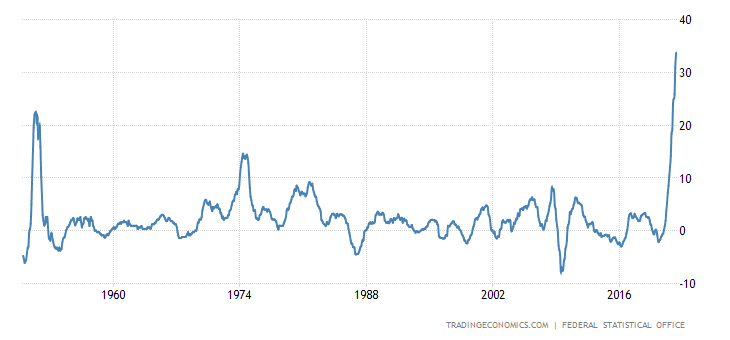

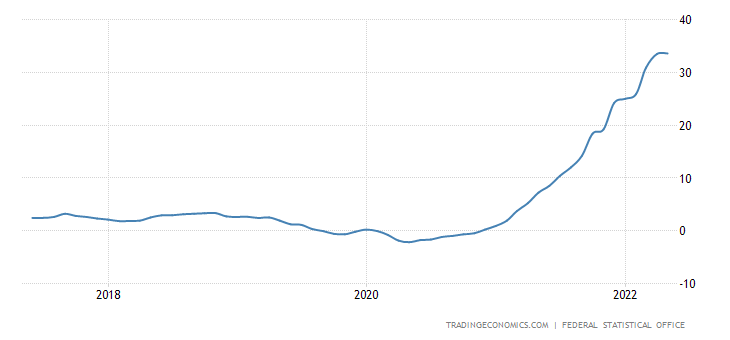

German PPI +33.6% per year peaked over 72.5 years of observations:

Germany Producer Prices Change

Germany Producer Prices Change

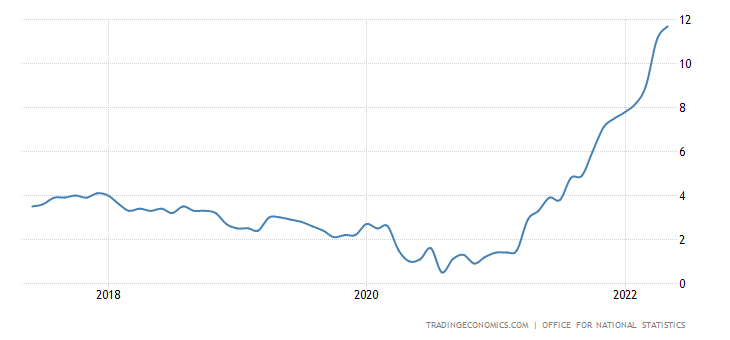

The US 30-year mortgage rate of 5.98% has been at its highest since 2008; add another 1% and there will be 20th-century levels:

United States MBA 30-Yr Mortgage Rate

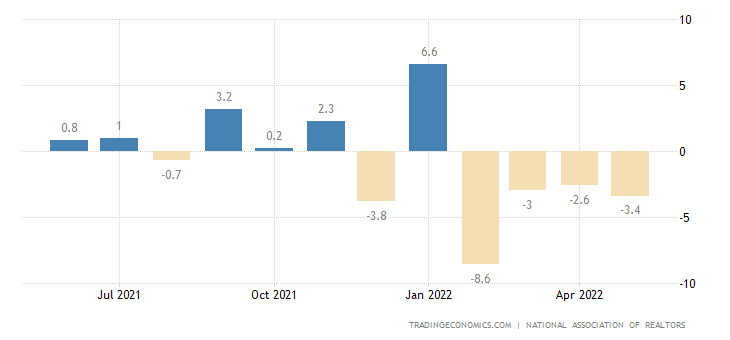

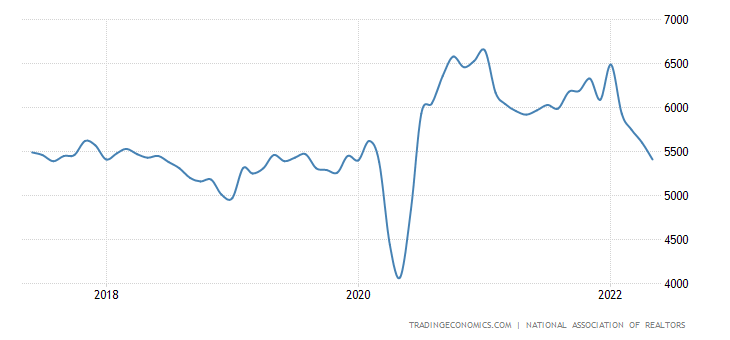

US existing home sales fall for 4 consecutive months:

United States Existing Home Sales MoM

Reaching a 2-year low:

United States Existing Home Sales

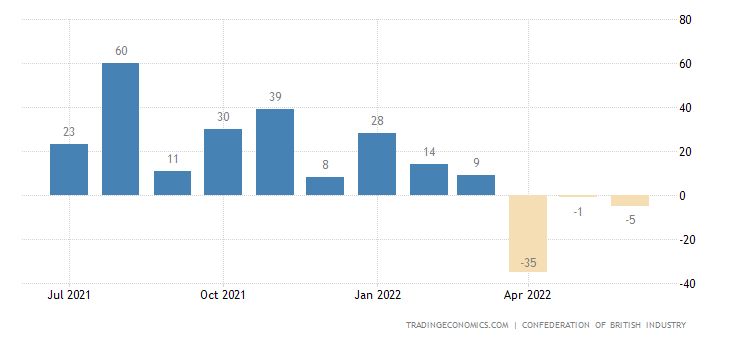

UK distributive trades keep in the red for 3 straight months:

United Kingdom CBI Distributive Trades

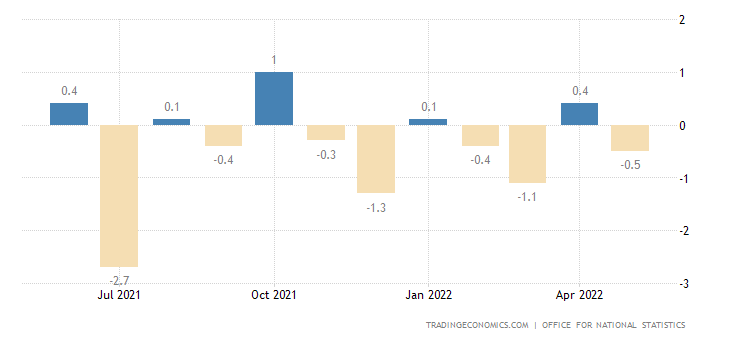

Retail sales themselves are falling and give out -0.5% per month:

United Kingdom Retail Sales MoM

And -4.7% per year:

United Kingdom Retail Sales YoY

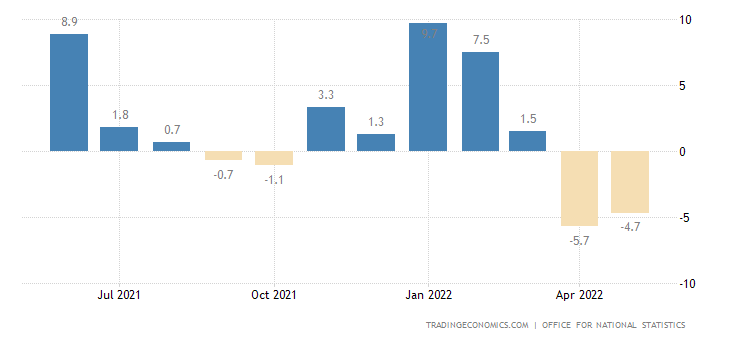

Excluding fuel, over the past year there were only 3 monthly positives:

United Kingdom Retail Sales Ex Fuel MoM

New Zealanders are extremely pessimistic over 34.5 years of data acceptance:

New Zealand Consumer Confidence

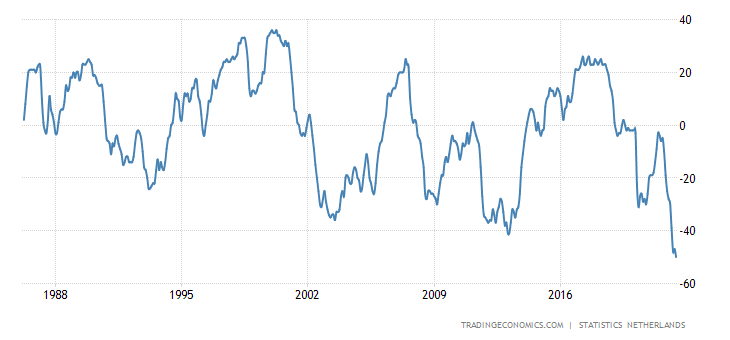

The same in the Netherlands, where pessimism reached a record high in 36.5 years of statistics:

Netherlands Consumer Confidence

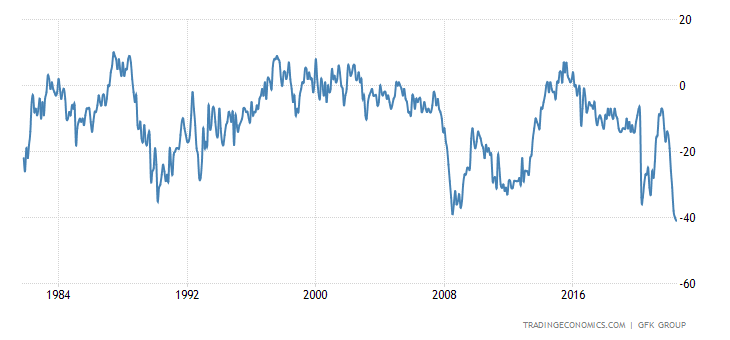

The British consumers are incredibly gloom (for 41.5 years of survey):

United Kingdom Consumer Confidence

United Kingdom Consumer Confidence

Not surprisingly, Johnson’s government is twitching at this: otherwise, explaining the situation to citizens becomes extremely difficult.

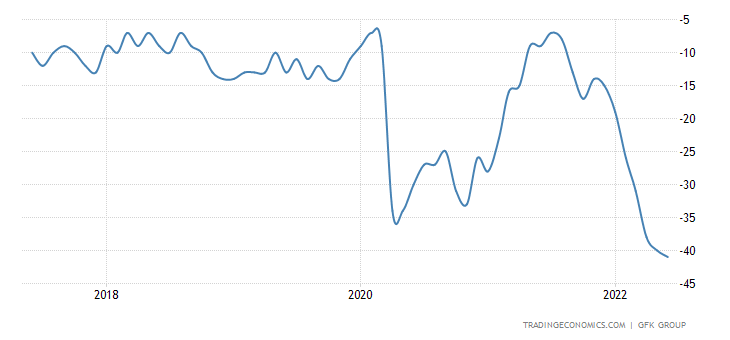

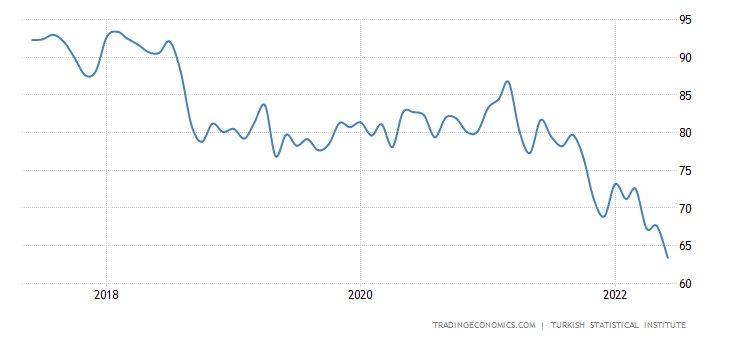

The consumer sentiment of the Turks is at a record low level:

Turkey Consumer Confidence

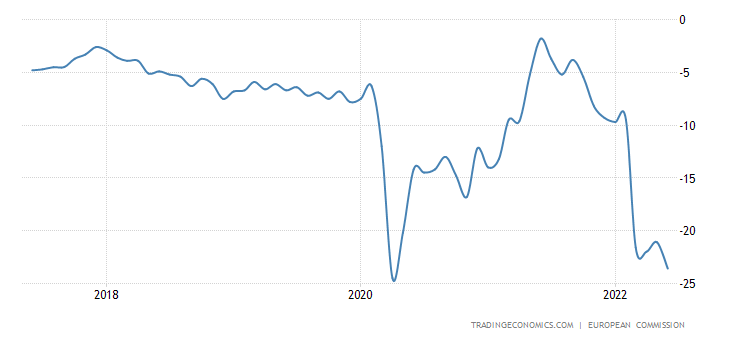

The Euro Area is close to the same:

Euro Area Consumer Confidence

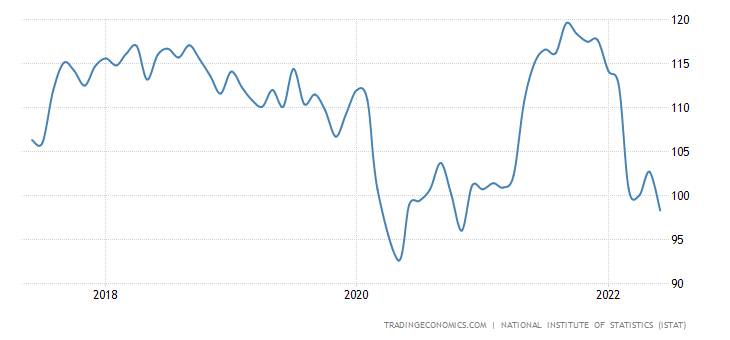

Consumer sentiment of traditionally optimistic Italians has gone into a two-year trough:

Italy Consumer Confidence

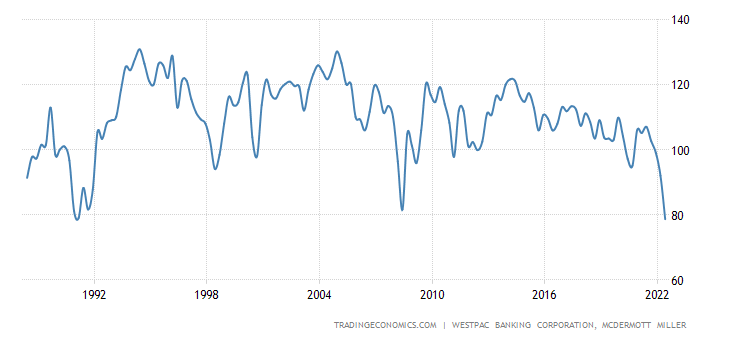

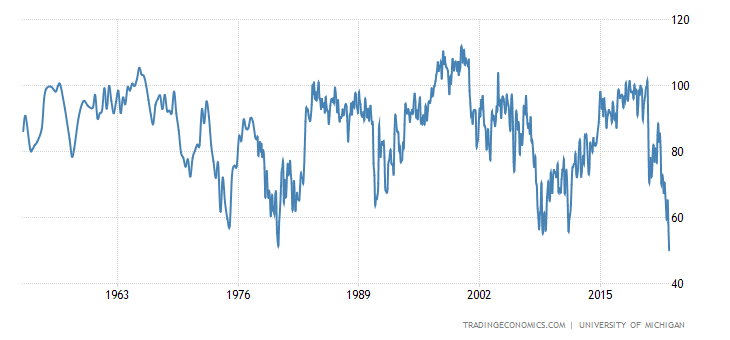

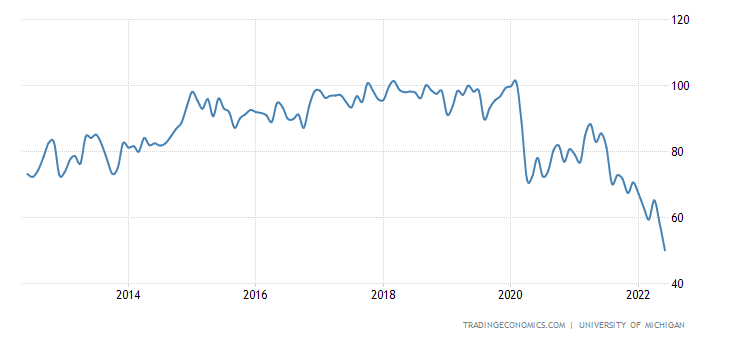

Finally, the United States Michigan Consumer Sentiment Indicator is the worst in 70 (!) years of observation:

United States Michigan Consumer Sentiment

United States Michigan Consumer Sentiment

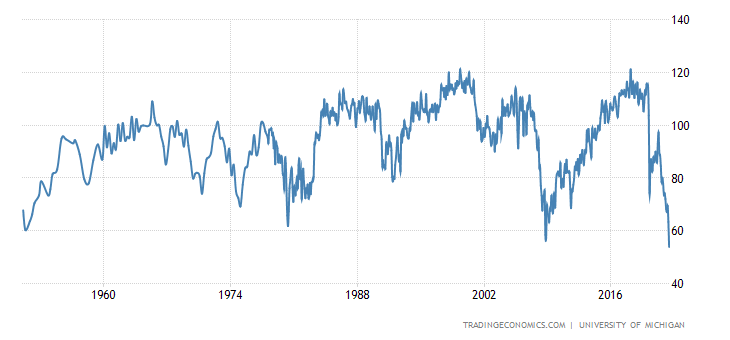

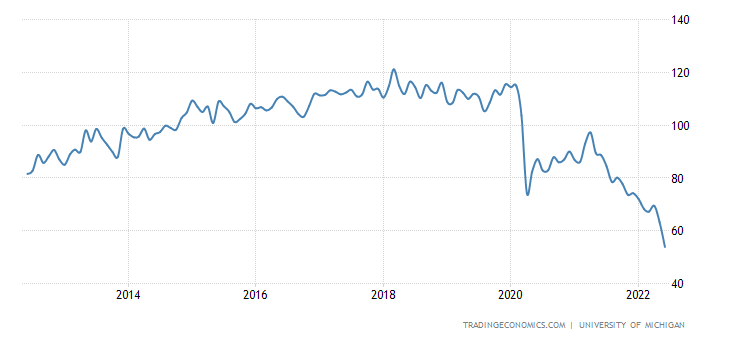

And everything is extremely overshadowed by the assessment of current conditions:

United States Michigan Current Economic Conditions

United States Michigan Current Economic Conditions

The Central Bank of China has left the previous monetary policy, new incentives do not seem likely.

Neither has the Indonesian Central Bank changed anything, but it is squeezing liquidity by increasing the rate of reservation.

All is still with the Central Bank of Turkey, but the Central Bank of Mexico hiked the rate for the 9th consecutive time, by 0.75% to 7.75%.

Summary

We see a canonical shift in the position of monetary (and political) authorities towards the admission of a deep and protracted crisis. As this process unfolds, both internal political disputes (which remain outside the focus of our purely macroeconomic analysis) and serious economic conclusions will begin.

The latter will inevitably include both hysterical political moves (for example, it is possible that someone from the Central Bank will simultaneously raise the rate and increase the issue) and perfectly reasonable actions related to debt relief. Including the removal of certain countries, for example, the eastern and southern members of the European Union.

From the point of view of the major players, this is a perfectly natural policy, but if the ideological opposition of recent decades (liberalism versus conservatism) is taken, it could mean the beginning of the most brutal purge of national elites in a large number of countries. And, with the global dollar system beginning to disintegrate, this could result in liberal loyalists in some African or Eastern European countries being forced to abandon their principles fairly quickly or to leave their countries for good. And, with the global dollar system breakdown, this could result in liberal loyalists in some African or Eastern European countries being forced to abandon their principles fairly quickly or to leave their countries for good. Given that it is impossible to remain a member of the elite in foreign countries, this will lead to a drastic reduction in the number of liberal elites worldwide.

By the way, if EU or US emissions resume, stock markets may still be seriously up. But in general — it will be the last paroxysms before the colossal collapse.

In addition, as the transition of liberal elites to conservative elites in Eastern Europe will occur fairly quickly (given the magnitude of the crisis), it is likely that a fairly serious border change will begin to simplify and legalize the process.

Since all the countries of Eastern Europe have no economic subjectivity at all, this means significant changes in economic relations and, consequently, financial flows.

Exhausted?")