The main news can be summarized in one phrase of the head of the Fed said at a press conference after the announcement of a 0.75% rate hike (nothing unexpected happened here): "The final level of interest rates will be higher than previously expected (September 21)."

The decrease in inflation can occur only after the end of the structural crisis in the modern dollar economy, which can happen no earlier than in a few years. At the same time, the monetary component of inflation will indeed be able to be reduced. Moreover, this is really happening:

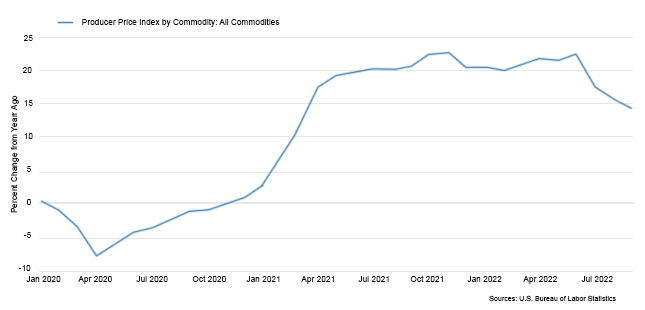

Of course, 15% is better than 23% (the maximum of industrial inflation at the beginning of the summer of this year), but, you see, this is far from the desired 2%. Note that we chose this indicator (growth in prices for the entire volume of industrial goods) for two main reasons. First, unlike the PPI index, it is not published in the public field. It means that one can hope that it is less prone to fraud. The second is that the totality of price indicators for all goods is more indicative than the set of final goods in production chains, which, moreover, are more dependent on purely market factors (demand of consumers external to the industry).

Moreover, if you look at the chart, you can see that the reaction of prices to the rate increase is gradually decreasing. It was sharp in summer and then began to decline. It is possible (and it is still a hypothesis) that the monetary component of inflation is already approaching zero, and the structural element is somewhere around 12-13%. And it will only grow from a further increase in the rate. We will know the results of October in two weeks, and the reaction to the last rate increase will be evident only by mid-December. So, it will be possible to test this hypothesis only by the end of the year.

Macroeconomics

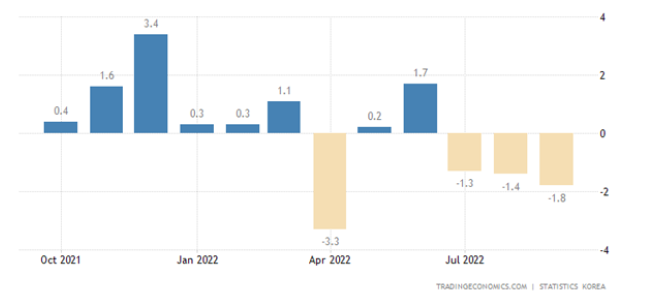

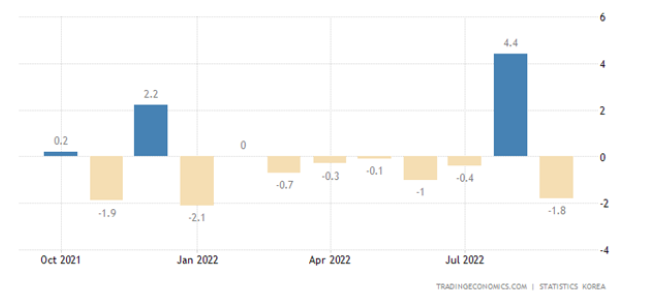

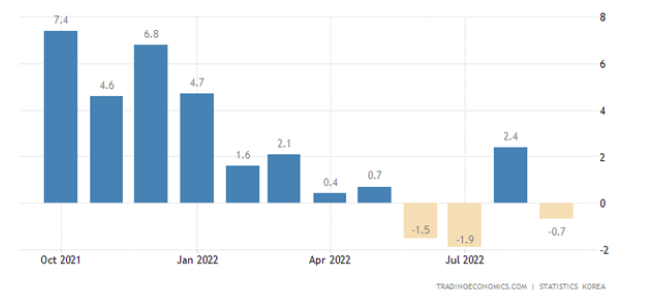

Industrial production in South Korea (-1.8% m/m) has been declining for 3 consecutive months:

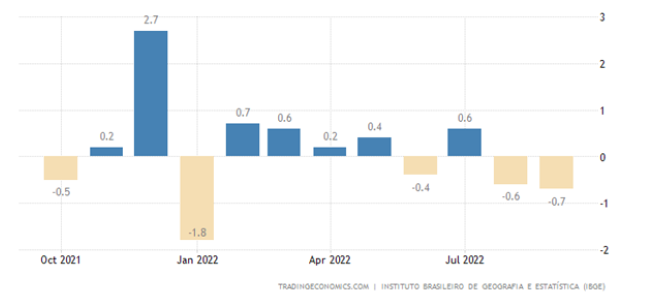

In Brazil – 2 consecutive months (-0.7% per month):

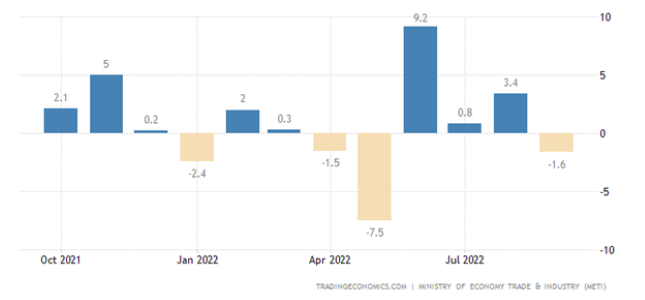

In Japan, industrial output also fell (-1.6% per month):

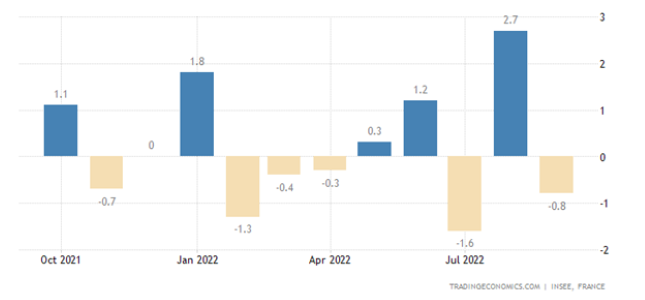

In France -0.8% per month:

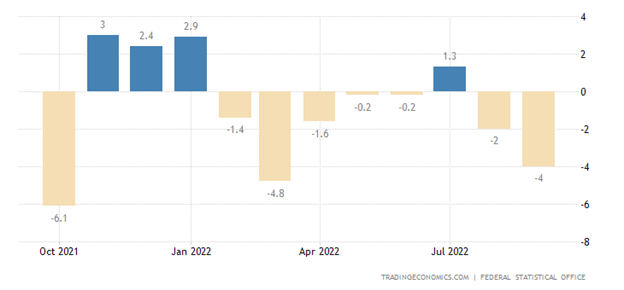

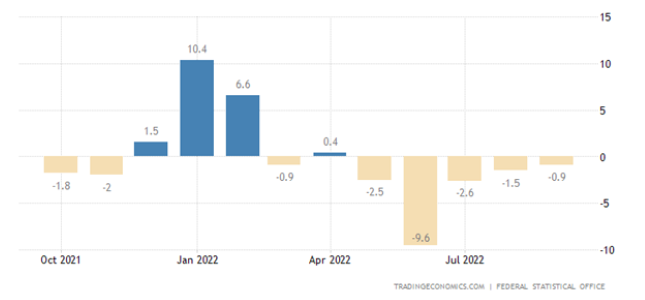

German factory orders -4.0% per month – 2nd negative in a row and 7th in the last 8 months:

And -10.8% per year — the 7th consecutive month of decline:

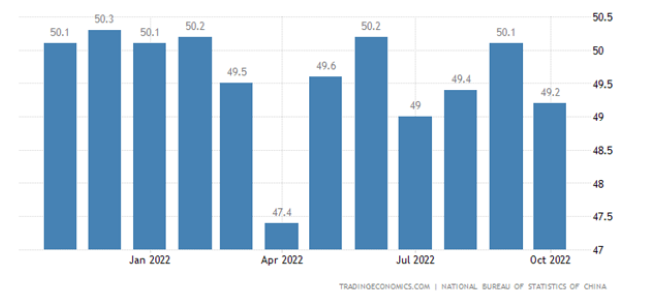

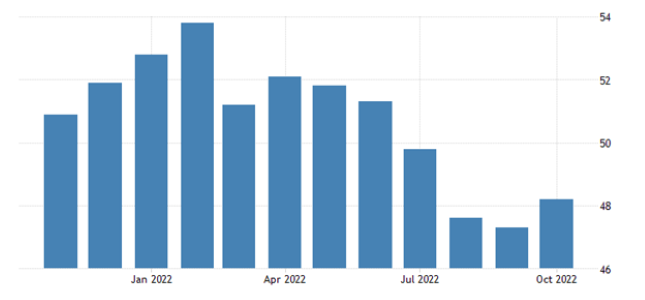

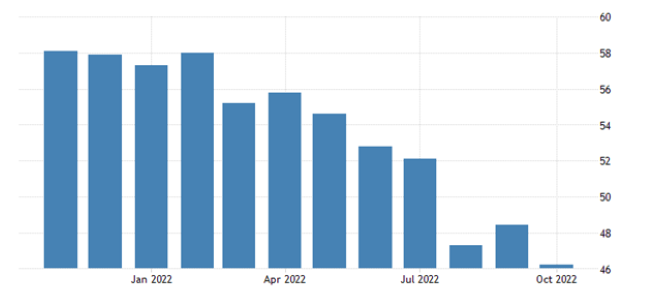

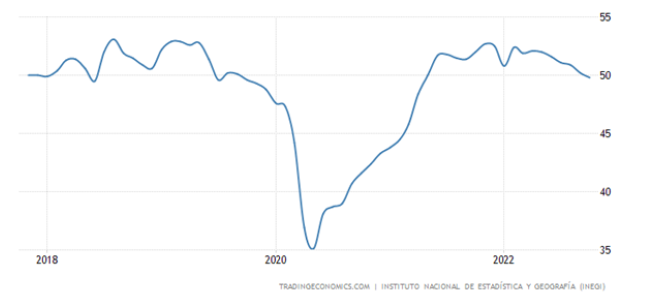

Official PMI (an expert index indicating the state of the industry; its value below 50 means stagnation and recession) of China returned to the recession zone in all sectors of the economy:

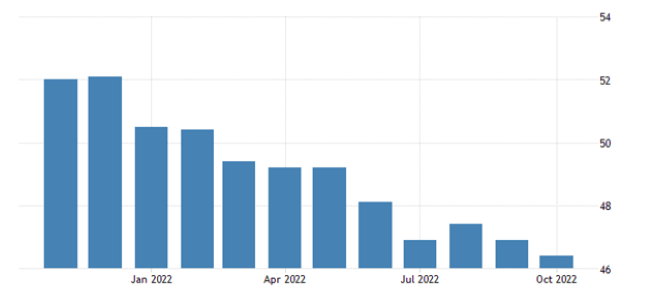

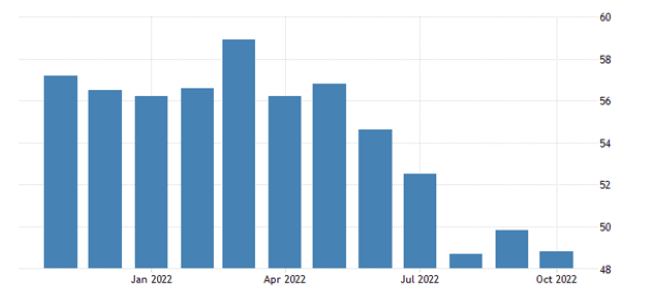

Independent estimates confirm the recession

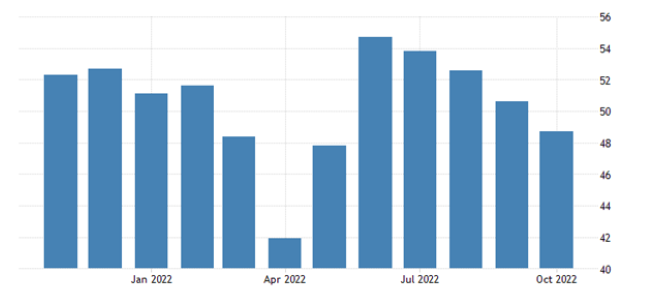

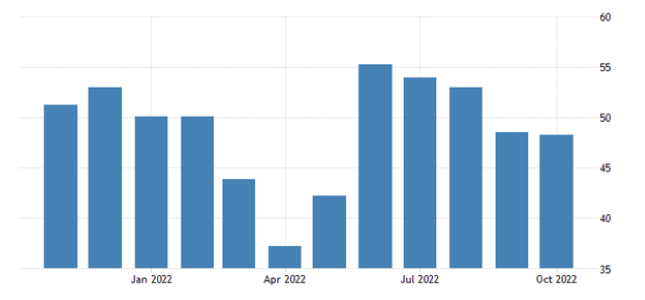

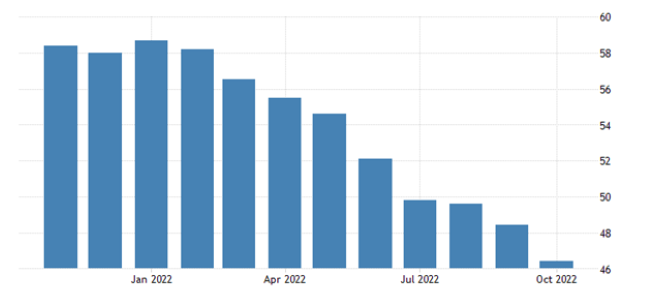

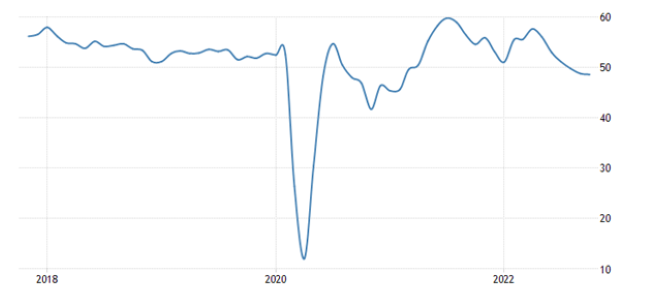

Manufacturing PMIs point to decline almost everywhere: in Australia (49.6):

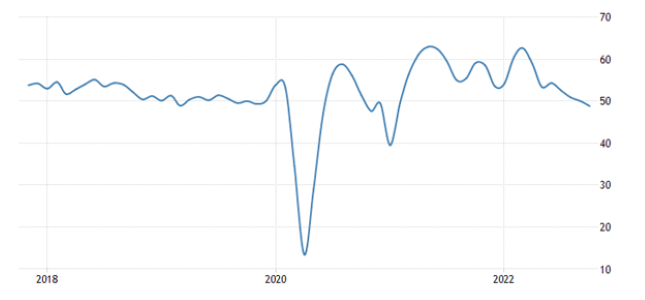

In South Korea (48.2):

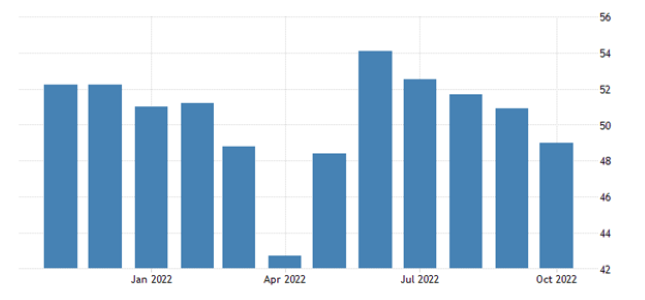

In Turkey (46.4):

In the Eurozone (46.4):

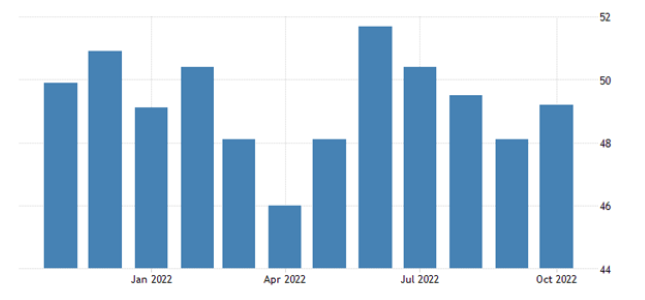

In Sweden (46.8):

In Britain (46.2):

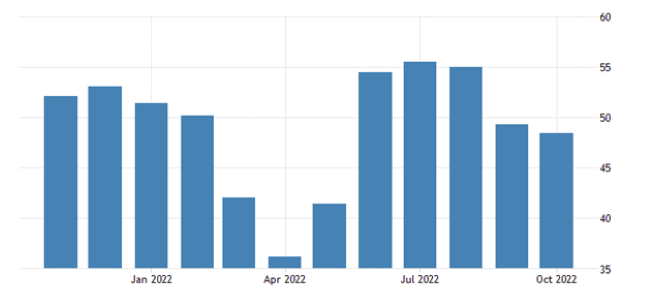

In Canada (48.8):

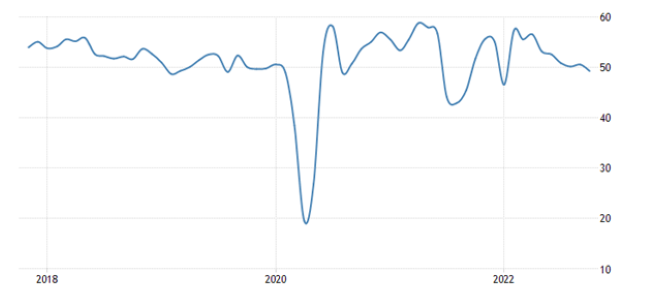

In Japan, there is still stagnation (50.7) – but still at least for 21 months:

The same in the US for both versions: 50.8 and 50.2, the lowest numbers in 28 months:

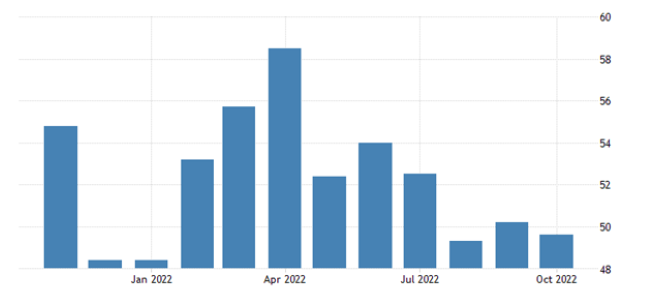

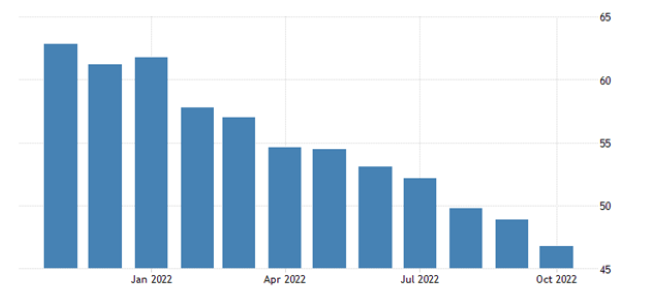

A similar picture in the services sector: in Australia (49.3):

In the Eurozone (48.6):

In the UK (48.8):

In the US (47.8):

Business confidence in Mexico at bottom in 1.5 years:

U.S. Midwest Manufacturing (Chicago PMI) decline intensifies to 28-month peak (45.2):

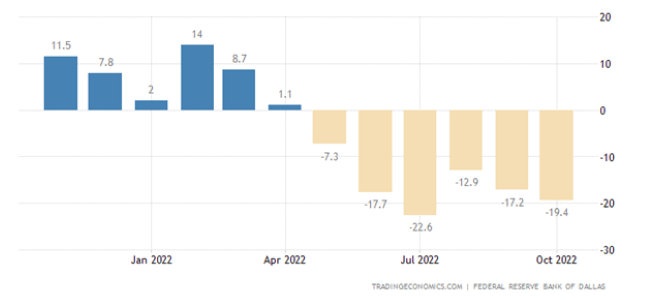

A similar indicator of the Texas Fed is in the red for 6 months in a row:

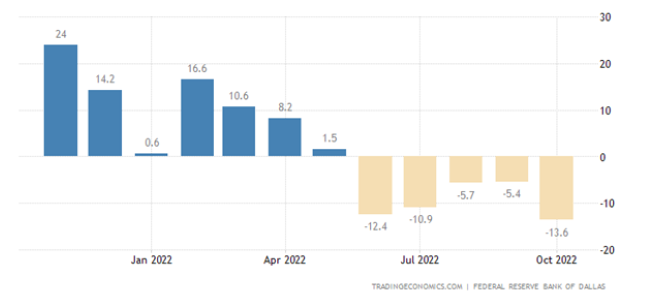

And his service sector index is 5 months:

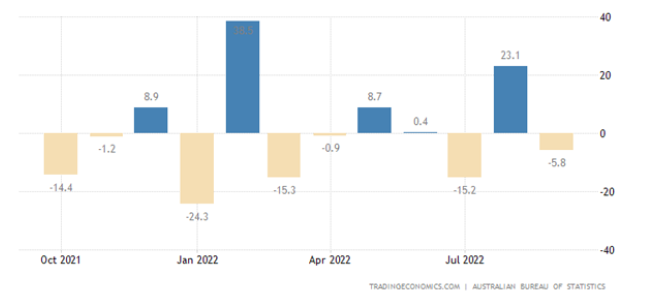

Building permits in Australia -5.8% per month and -13.0% per year:

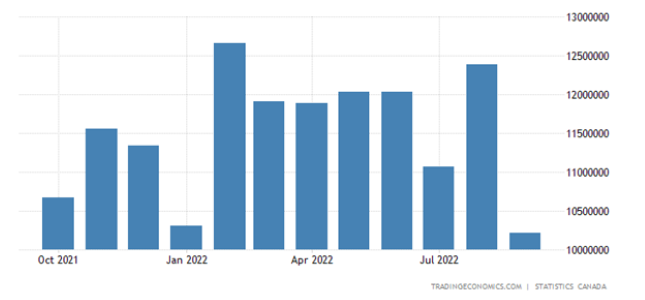

And in Canada -17.5% per month:

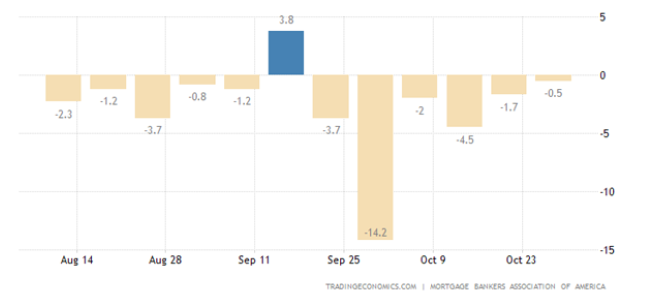

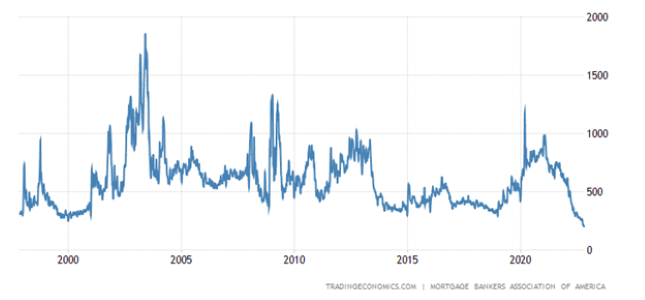

US Mortgage Applications Fall For 6th Week In A Row Despite Mini Loan Rate Cuts:

And updated the 25-year low:

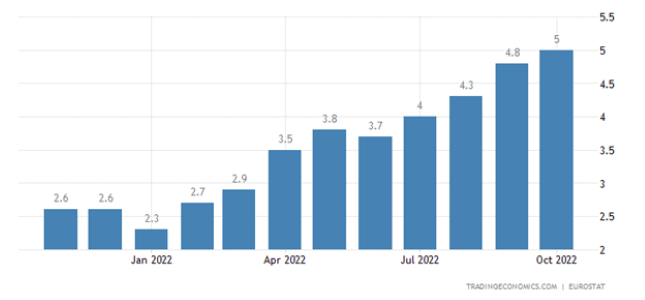

Eurozone CPI (Consumer Inflation Index) +10.7% per year – a record for 32 years of observation:

Record and “clean” (minus highly volatile components of food and fuel) CPI (+5.0% per year):

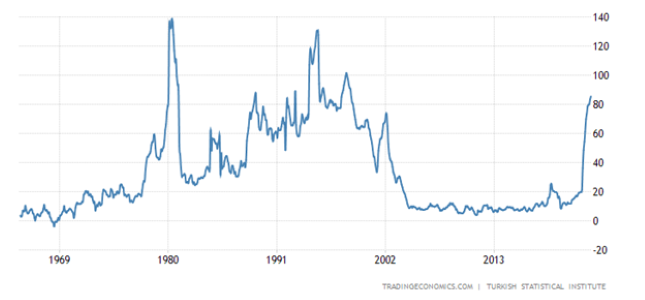

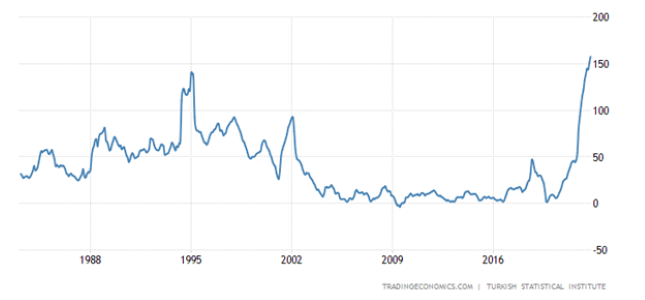

Turkish CPI +85.5% per year – maximum since 1998:

PPI (industrial inflation index) Turkey +157.7% per year – a record for 40 years of data collection:

Retail South Korea -1.8% per month – over the past year there were only 3 pluses:

Why did the annual dynamics go negative (-0.7%):

In Germany, the annual decline in retail is observed for 5 months in a row:

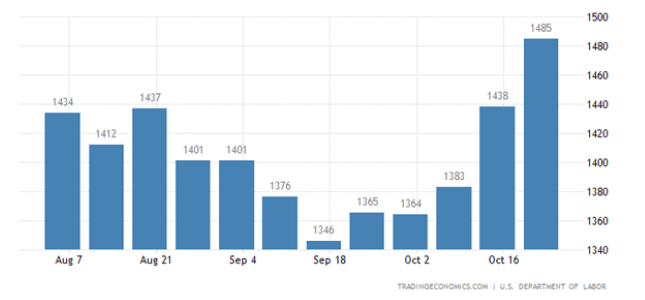

Number of U.S. Unemployment Claims in 7 Months Maximum:

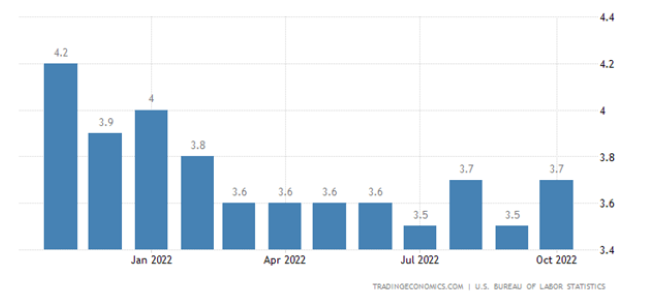

And the unemployment rate for 8 months:

The Fed raised the interest rate by 0.75% to 3.75-4.00%.

As usual, the Central Bank of Saudi Arabia follows the path of the Fed (+0.75% to 4.50%). The Bank of England also increased the rate by 0.75% (for the first time in 33 years) to 3.00%. The Central Bank of Australia raised the rate by 0.25% to 2.85%.

Main conclusions

Why do we have such a significant impact on raising the rate, after all, in 1981, the rate reached, albeit for a short time, 20%, and 19% was quite a long time. And here's why:

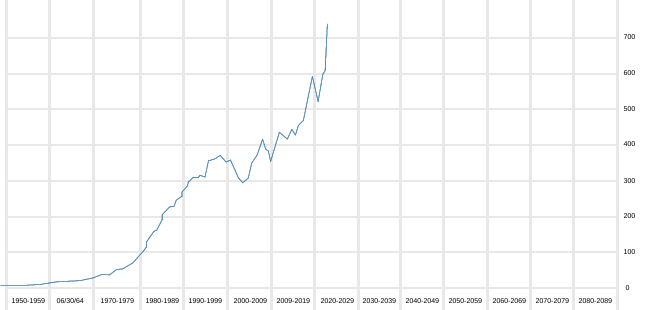

This is a graph of the cost of servicing the US government debt. As you can see, the situation is similar for corporate debt and household debt. And the household debt itself is almost twice as much as it was in 1980. Corporations are even worse off. For this reason, everyone understands that a further increase in the rate will inevitably cause massive bankruptcies and the collapse of financial markets.

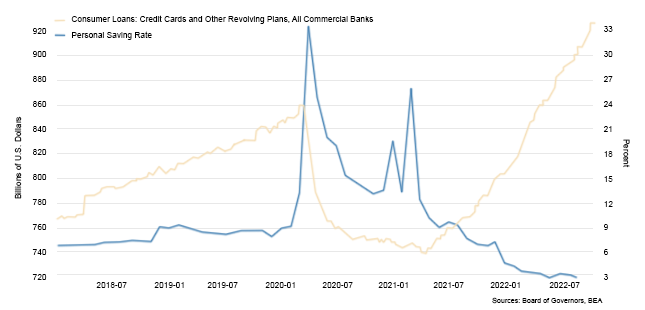

It should be noted that the debts of households, which fell after 2008, have recently begun to grow again. Just look at the credit card debt that is being called upon when average debt is already becoming difficult to increase:

Why raise the rate in such a situation? And the fact is that these banks can ideally exist in conditions of high inflation. But the real sector, industry, cannot exist like that. And so, Powell's aggressive rhetoric means that of the banks and industry, the sector may have been chosen to save. Let's see what Powell said.

– Inflation expectations are under control (has been on a downward trend for the past three months), but the longer high inflation continues, the more likely it is that higher inflation expectations will take root.

– The inflation target is unchanged and remains at the level of 2%. The Fed intends to fulfil its obligations to bring inflation back to the target.

– The Fed will take decisive steps to normalize demand in line with supply.

– The critical task is to stabilize inflation expectations and reduce actual inflation.

– Financial conditions have tightened significantly, which is reflected in the most vulnerable sectors, such as real estate.

– It will take time to fully feel the impact of monetary restrictions (especially on inflation).

– Further actions will depend on the totality of incoming data. The Fed will consider the combined effect of monetary policy tightening and the delay (lag) in the transmission of monetary policy on economic activity and financial stability.

– The monetary policy first affects financial conditions, then influences economic activity and financial stability, and already at the third stage, it directly affects inflation itself. This lag can be substantial, but it is important to note that economic conditions are set ahead of the Fed's immediate action. Thus, DCT transmission in current conditions is faster than in the 80s.

– It would be prudent to slow down the pace of tightening monetary policy when the interest rate becomes "restrictive enough" to push inflation towards the 2% target. There is considerable uncertainty around this interest rate level, and the Fed has no idea where this "restrictive level" is located.

– The final level of interest rates will be higher than previously expected (September 21).

– Reducing inflation is likely to require a long period of below-trend economic growth and degradation of labour market conditions.

– Historical data warn against a premature weakening of monetary policy. The Fed will stay tight until inflation returns to its target.

– There is no universal benchmark by which it will be apparent that a trigger has come to stop the cycle of tightening the PrEP. A decrease in inflation in several inflation reports will not be a reason to revise the monetary policy. The Fed will use a mix of financial and macroeconomic indicators to ensure inflation is on a sustainable path to the target.

– How far should we go with the tightening of PrEP? The pace of monetary tightening is extreme, but it is in response to an unprecedented inflationary momentum. Concerning the cap level of the rate, the cap level will be such that there is sufficient reason to believe that the inflationary trend has reversed. This level is indeterminate. The Fed still has a lot to do in this direction. Strong macro data would suggest that rates could be higher than previously expected.

– The Fed has no decision on when to slow down the rate of rate hikes. It could be December 14, or it could be February 1. The more important question is how much to raise rates and how long to keep them at a high level.

– In constructing its monetary policy, the FRS will focus more not on the actual level of inflation but on the forecasted level of inflation and from it to calculate actual rates in the money market. The Fed may view actual favourable rates as an intermediate goal, but it is not an end.

– Many households and businesses are already taking loans at rates that are close to inflation or higher than inflation, so we can assume that at the moment, actual rates are already in the positive area.

– From the point of view of the balance of risks, the losses from the rapid tightening of monetary policy are less significant than the costs of losing control over inflation.

– The housing market is overheated; there was a bubble. Falling prices and falling sales are regular, but there is no bubble in the subprime lending market like there was in 2007, and the situation is generally manageable in terms of the quality of the loan portfolio.

– A strong dollar is a problem for many countries (those with significant foreign debt denominated in dollars or a high proportion of imported raw materials).

– If the Fed is overdoing it with tightening, the Fed has the tools to fix it (Powell snidely refers to the March 2020 experience with unlimited liquidity bazooka).

– Discussing a pause in tightening is premature. Inflation is not where it should be, and we still have to find a "restrictive level" of the interest rate at which supply and demand will normalize.

– Containment of public spending manifested itself not as we would like. Consumers continue to spend actively, associated with accumulated savings in 2020-2021.

– There was a narrowing of the path to a soft landing due to the trajectory of tightening the monetary policy (the first recognition of a potential crisis from Powell).

– Everything went wrong, as predicted by the Fed. Inflation is not declining as it should be, the labour market remains strong when it should have begun to fall, and demand is still strong while supply growth is limited.

– The Fed is committed in its intentions to bring inflation under control.

The general conclusion consists of several points. First, Powell admitted the obvious: the Fed was seriously mistaken in assessing the inflation situation. By the way, the management of the FRS still lacks a fundamental understanding of high inflation. It still does not understand the essence of the structural crisis.

Secondly, Powell sent severe forces to restore the authority of the Fed. Never before have his predecessors explained in such detail and clearly what they are doing and why. Clearly, the aforementioned leaders did not particularly admit their mistakes, but, of course, they did not come close to such disgrace as they are now. Whether Powell will be able to resolve this issue, especially given the conclusion at the end of the previous paragraph, we do not know. Moreover, we seriously doubt it.

Thirdly, the question is political. There were two basic scenarios, saving the world dollar (Bretton Woods) system at the cost of the remnants of the real sector of the American economy or saving this real sector of the US economy at the expense of the Bretton Woods systems. Powell's press conference seems to hint that a second decision has been made (very late).

The final result will be seen in the coming months!

Exhausted?")