The main news of the week was the decision of OPEC to reduce oil production. The hysteria in the US is understandable, since the main thing here is not oil prices (actually, oil prices are not the main problem in the US today), but the fact that members of the organization pointedly ignored US interests.

Yes, we have repeatedly noted that the most adequate leaders of the countries of the world (current and former) note that the old economic and political models no longer work (“the old order cannot be returned”). So, over the past week, Merkel, who has been the chancellor of Germany for so long, has been noted twice that her opinion is always important. So, she first said, and then repeated, that it is necessary to build a new security architecture for Europe, and together with Russia.

It should be noted that the security of Western Europe, and then the whole of Europe, was provided precisely by the United States, but today it is already clear that they are not entirely successful in this (the OPEC decision is proof of this). Moreover, security is not only political, but also economic and financial. And with the latter, everything is very bad. Of course, the current politicians of the European Union (with the exception of the head of Hungary, Orban) operate within the framework of the old order, but it is already becoming clear to everyone that it has come to an end.

The trouble is that within the framework of the old order, the new one has not yet been born. And this means that the crisis is getting worse all the time and will get worse. However, let’s hope that our advice will help subscribers to pass it with minimal losses.

Macroeconomics

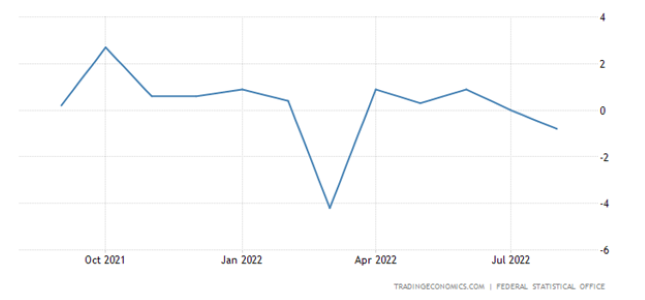

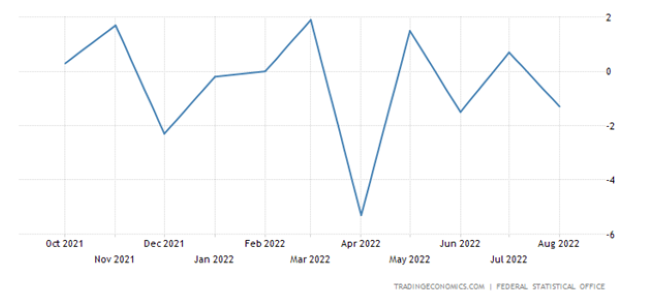

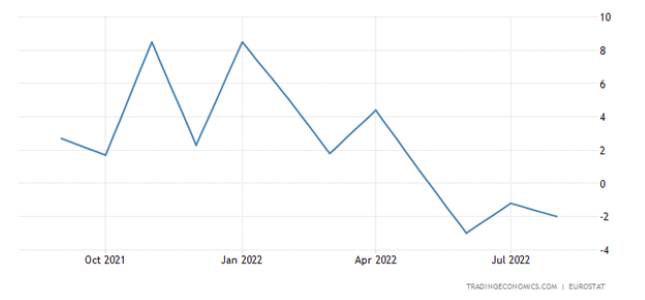

Industrial orders in Germany -2.4% per month – the 6th minus in the last 7 months:

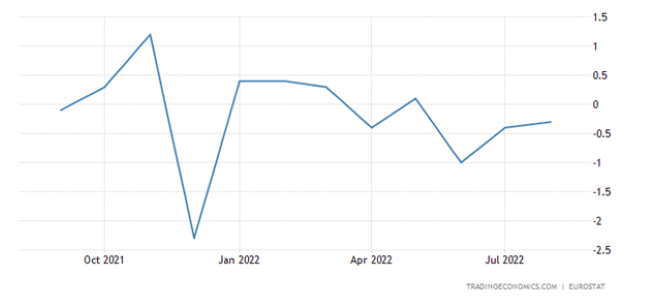

And -4.1% per year — the 6th negative in a row:

And industrial production in Germany also went into the red:

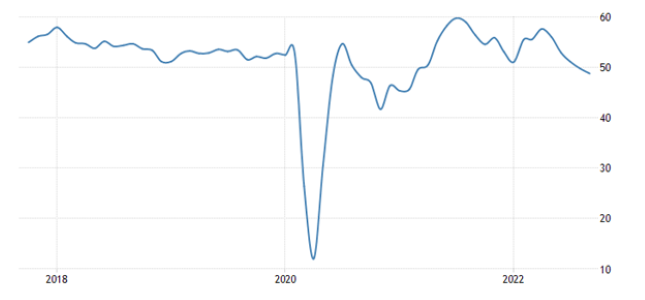

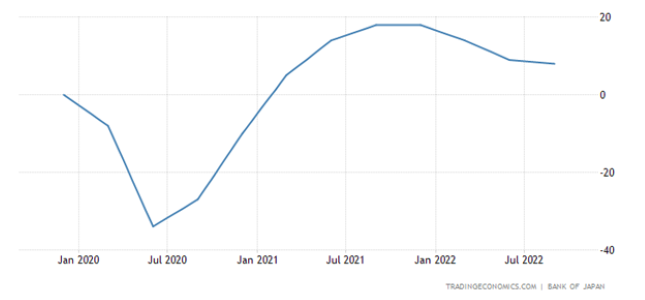

PMI (expert index of the state of the industry; its value below 50 means stagnation and decline) of Japan at the bottom for 20 months:

In South Korea, in 26 months and in the recession area:

In Sweden – in 27 months and also in the recession zone:

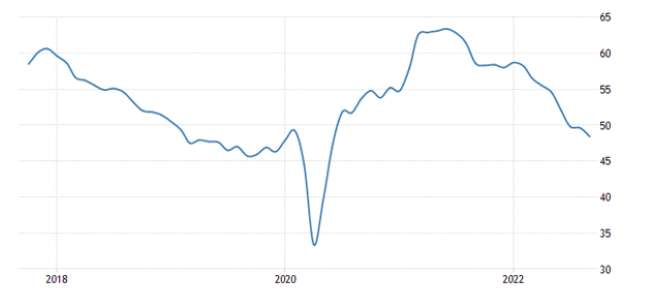

In the euro area as a whole, the picture is similar:

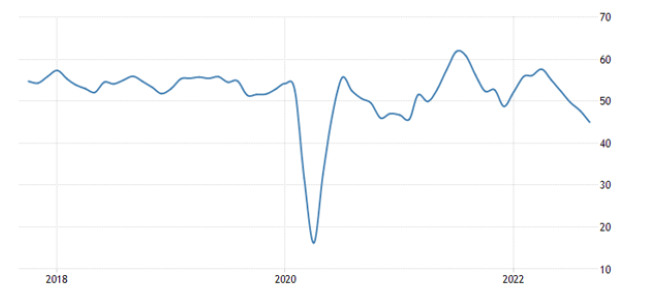

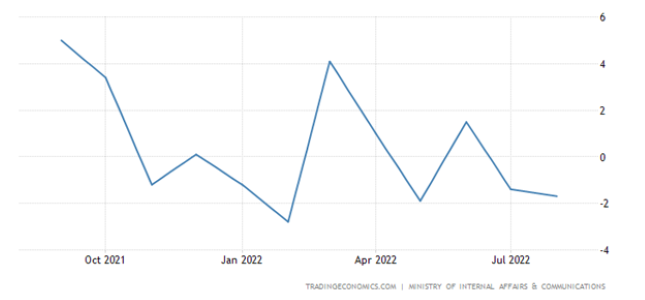

A similar situation in Turkey:

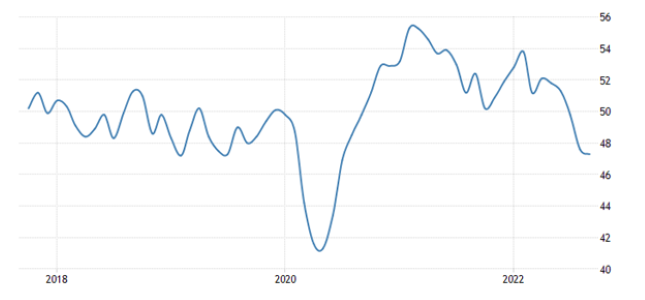

The 27-month bottom is also in the USA, but so far there is only a stagnation zone (of course, taking into account the underestimated inflation, most likely, the decline in the USA has been going on since the fall of last year, 2021):

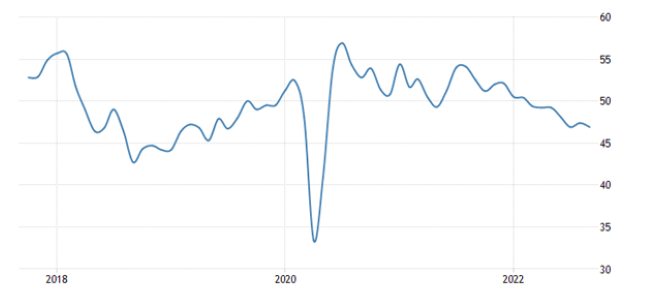

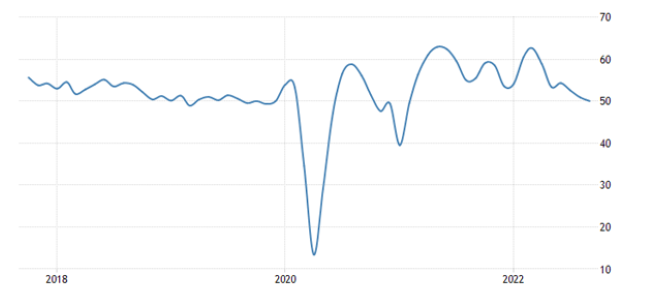

Eurozone services PMI in decline zone and at the bottom for 19 months:

Including in Germany – for 28 months and very low (45.0 points):

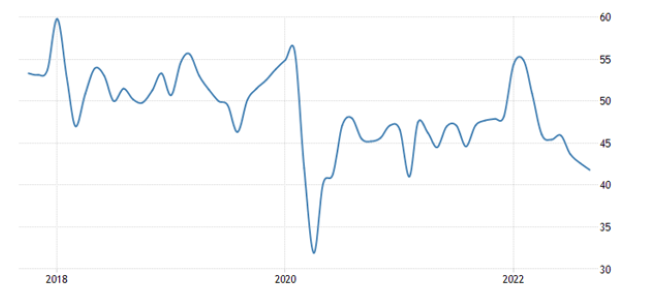

UK stagnant and 19-month low:

German construction PMI is in the depression zone (41.8 points) and is the lowest in 19 months:

It is not surprising that Merkel began to make her statements, and the hysteria of the current leadership of Germany is understandable. Another thing is that this hysteria is not aimed at problems with the country’s economy, but at the fight against Russia.

The mood of major manufacturers in Japan is the worst for 1.5 years:

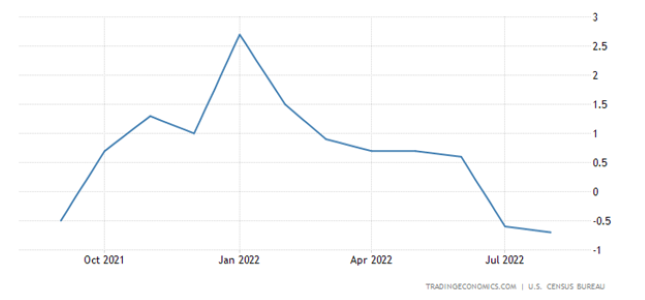

Construction spending in the US showed the 2nd consecutive monthly loss:

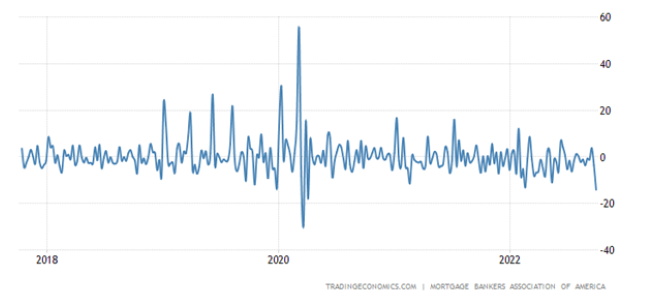

Mortgage applications in the US -14.2% per week – the worst dynamics since April 2020:

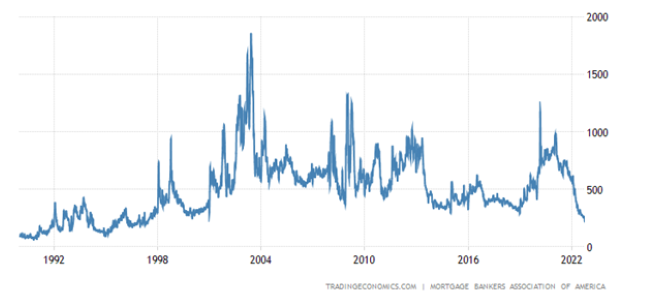

To a minimum since 1997:

As the mortgage rate approached its 2006 peak:

This is about inflation in the US, see the next section of the Review.

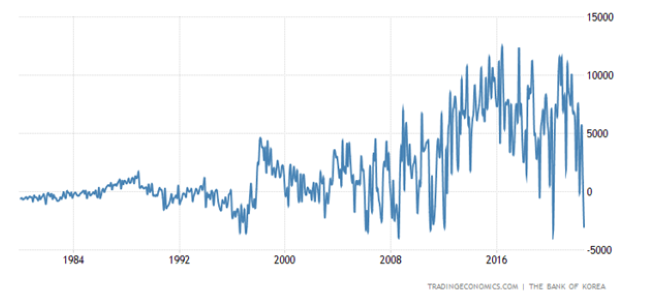

South Korea’s current account is close to historical anti-records:

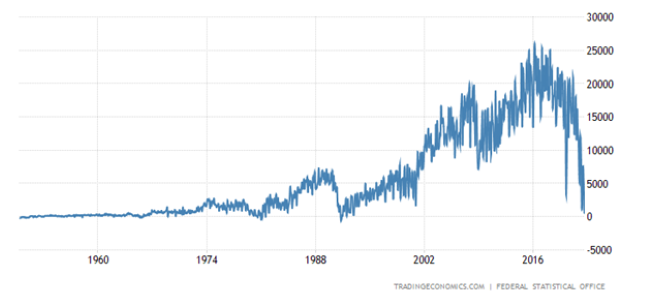

Germany’s foreign trade surplus is the smallest since January 1992:

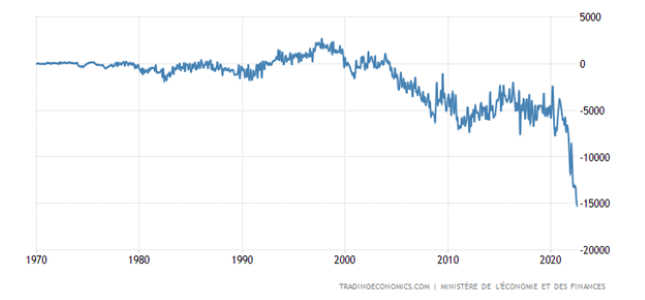

And in France, a record deficit in 53 years of observations:

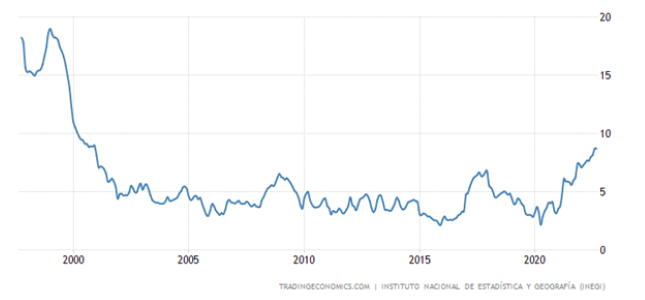

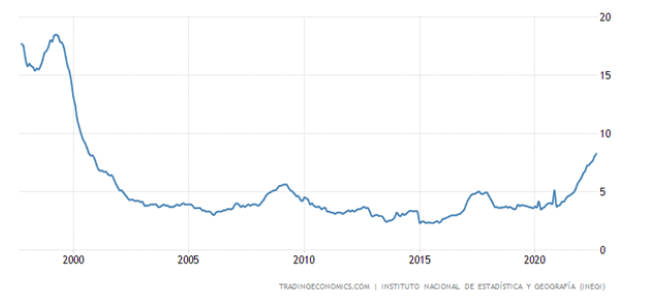

CPI (Consumer Inflation Index) of Mexico remained at the 22-year high of +8.7% per year:

And the “net” (excluding highly volatile food and fuel components) CPI updated the same peak (+8.3% per year):

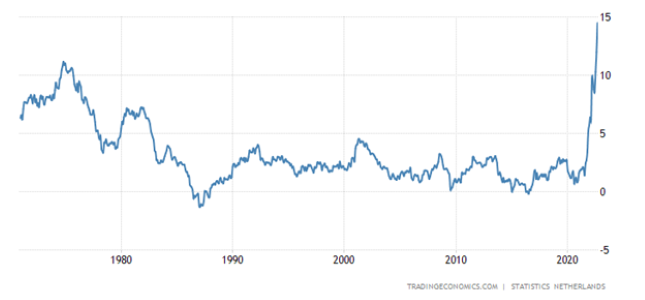

CPI of the Netherlands +14.5% per year – a record for 52 years of statistics:

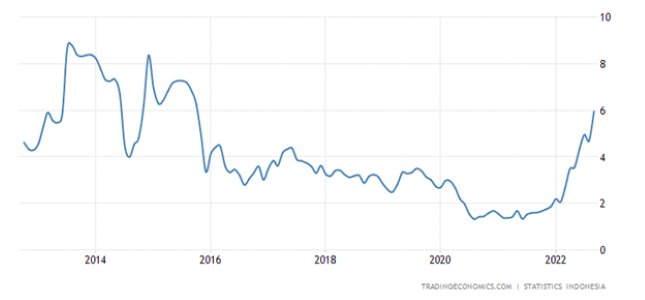

Indonesian CPI +5.95% p.a. – 7-year high:

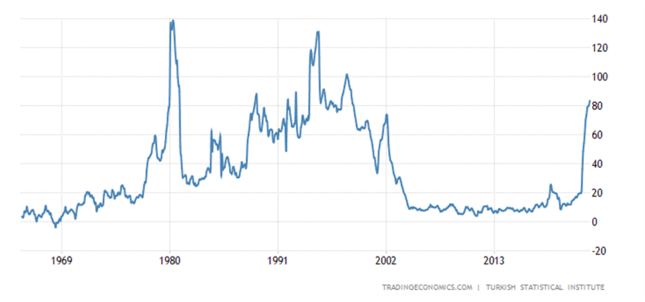

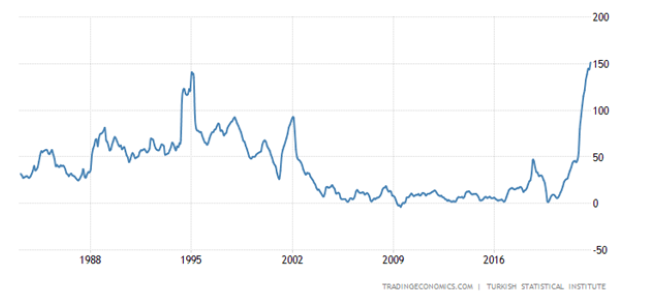

Turkish CPI +83.5% per year – peak since 1998:

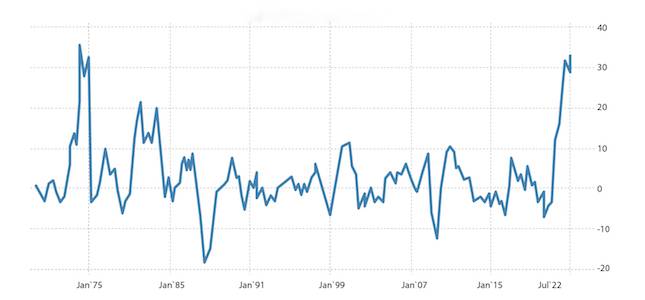

Turkey’s PPI (industrial inflation index) +151.5% per year – a record for 40 years of observation:

Eurozone PPI +43.3% per year – also a record for 40 years of data collection:

Import prices in Germany + 32.7% per year – they were slightly higher only in March-April 1974:

Retail sales in Germany -1.3% per month:

And -4.3% per year — the 4th negative in a row:

Eurozone retail -0.3% m/m — 3rd negative in a row:

And -2.0% per year – also the 3rd negative in a row:

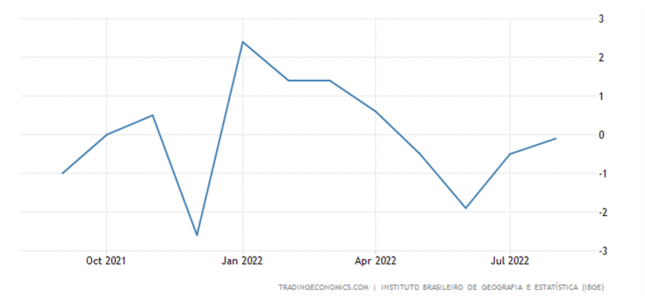

Brazil Retail Declines Monthly for 4 Months in a Row:

Japanese spending in monthly minus 2 months in a row and 3 of the last 4:

Job openings in the US declined at the worst rate in 2.5 years:

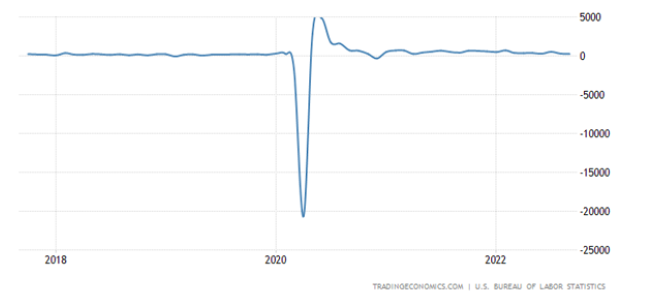

And the economy created the minimum number of jobs in 1.5 years (263 thousand):

This is about inviting German businesses to the US. If they don’t want to invest their own, why should the Germans want it?

The US savings rate returned to the record lows of 2008 (3.5%, in June it was even 3.0%):

It should be noted here that after 2008, the methods for assessing savings in the United States changed, as a result of which indicators of the order of -5% – -7% (which estimated savings before the crisis) became positive. So now, most likely, the reality is somewhat worse than the official indicators.

The Central Bank of Australia raised the rate by 0.25% to 2.60% instead of the expected +0.50%.

Main conclusions

It seems that the dynamics of the structural crisis has even somewhat accelerated. No wonder the US Federal Reserve is so nervous, here is the opinion of Fed Board member Christopher Waller:

– I support further rate hikes until we see meaningful and sustained progress on US inflation;

– In the second half of 2022, the US economy will grow below the trend;

– The labor market is strong and extremely tight;

– The main goal of monetary policy should be the fight against inflation;

– Inflation is too high and unlikely to fall quickly;

– It’s hard to imagine that the economic outlook will change before the next Fed meeting;

– In November, the Fed will hold a very meaningful discussion on the pace of rate hikes;

– I predict that rate hikes will continue until early 2023;

– We have not yet made significant progress in the fight against inflation;

– To contain demand, the Fed must continue to raise interest rates;

– I’m analyzing the data to determine the appropriate pace of tightening.

– I am not considering slowing down or stopping rate hikes due to financial stability issues;

– Monetary policy can and should be aggressive to reduce inflation;

Before the November meeting, it is unlikely that there will be enough data to significantly change my economic forecast.

Once again in plain language: inflation will not fall yet, why neither I nor anyone else from the Fed leadership understands why it is growing, but we will discuss it. Unfortunately, inflation has a bad effect on the labour market, but we still don’t know what to do about it.

We can only note that the readers of our reviews know the answers to all these questions, which gives them a serious competitive advantage. And, in addition, we suspect that the current composition of the Fed’s leadership will not figure out what the problem is. Let’s go back to Western Europe. The situation there is difficult not only in the economy, but also in the financial sector. A couple of weeks ago, as we wrote, the British financial system almost collapsed. And the situation is not improving yet, and in continental Europe it is approaching the British:

Problems continue with European banks, including the three most problematic, Credit Lyonnay, Deutsche Bank and Credit Suisse (the picture refers specifically to the latter):

Well, as for the prices for gas and oil, then here we are just not inclined to panic. The fact is that both gas and oil will be enough if part of the production is stopped. So the European Union will solve its problems with fuel and energy – by leaving the position of the world industrial leader.

Exhausted?")